10 IOLTA Compliance Mistakes That Trigger Bar Complaints

Updated November 2025

Most IOLTA account violations aren't fraud. They're administrative errors made by well-intentioned attorneys who don't realize they're breaking the rules.

One transfer made too early. One reconciliation skipped. One client ledger that goes negative. That's all it takes to trigger a bar complaint, audit, or disciplinary action. If you need a practical refresher, LawPay offers a helpful overview of managing IOLTA accounts and complying with modern financial institutions' expectations.

This guide covers the 10 most common IOLTA compliance mistakes, why they're violations, and how to fix them before they become problems.

1. Transferring Funds Before They're Earned

The Mistake

You receive a $5,000 retainer and immediately transfer it to your operating account because "you know you'll do the work." Or you transfer fees when you send an invoice rather than when you complete the work.

Why It's a Violation

Funds in trust belong to the client until you earn them. Transferring unearned fees is conversion of client funds - even if you eventually do the work. The timing must match the earning, not the billing or your cash flow needs.

Real Example

Attorney receives $10,000 flat fee for estate planning. Transfers entire amount to operating immediately. Completes work over three months. During those three months, the unearned portion should have stayed in trust. Bar complaint filed after client review of trust records.

How to Fix It

Only transfer funds when work is actually completed - not when you bill, not when you need cash. For flat fees, transfer as you complete milestones. For hourly work, transfer after time is recorded and work is done.

Prevention

Implement a policy: no trust-to-operating transfers without documented completion of work. Review your billing system to ensure it tracks earned vs. unearned portions of retainers.

2. Negative Client Ledger Balances

The Mistake

You transfer $2,000 to operating for Client A's fees, but Client A's ledger only shows $1,800. The extra $200 came from another client's funds in the pooled IOLTA account.

Why It's a Violation

Using one client's money to pay yourself for another client's work is misappropriation. Even if you "fix it later" when Client A makes another payment, you've still violated trust rules.

Real Example

Solo attorney reconciles trust account monthly but doesn't check individual client ledgers before transfers. Discovers negative balances during annual review. Bar audit reveals pattern spanning 18 months. Result: public reprimand and required trust accounting training.

How to Fix It

Check the specific client ledger balance before every transfer. If the ledger shows $500, you cannot transfer $501—even if your total trust account has $50,000.

Prevention

Configure your practice management software to flag or prevent negative client ledgers. Review all client ledgers monthly during reconciliation. Never transfer "from trust" generically - always specify which client's funds.

3. Skipping Monthly Reconciliation

The Mistake

You reconcile quarterly, annually, or "when you get around to it" instead of monthly. Or you reconcile the bank account but skip the three-way reconciliation that matches bank balance, trust ledger, and client ledgers.

Why It's a Violation

Most state bars require monthly reconciliation. More importantly, problems compound. A $100 error in month one becomes a $5,000 unexplained gap by month six. You can't prove compliance if you're not reconciling.

Real Example

Small firm reconciles "every few months when it's convenient." Bar audit request arrives. Firm scrambles to reconcile 14 months of transactions in two weeks. Discovers $8,000 discrepancy they can't explain. Investigation follows.

How to Fix It

Complete three-way reconciliation by the 10th of every month. Match your trust bank statement, your trust ledger balance, and the sum of all client ledger balances. All three must equal.

For a complete walkthrough, see our IOLTA trust accounting guide.

Prevention

Put reconciliation on the calendar as a recurring task. Assign it to a specific person. Don't close your books each month until trust reconciliation is complete and documented.

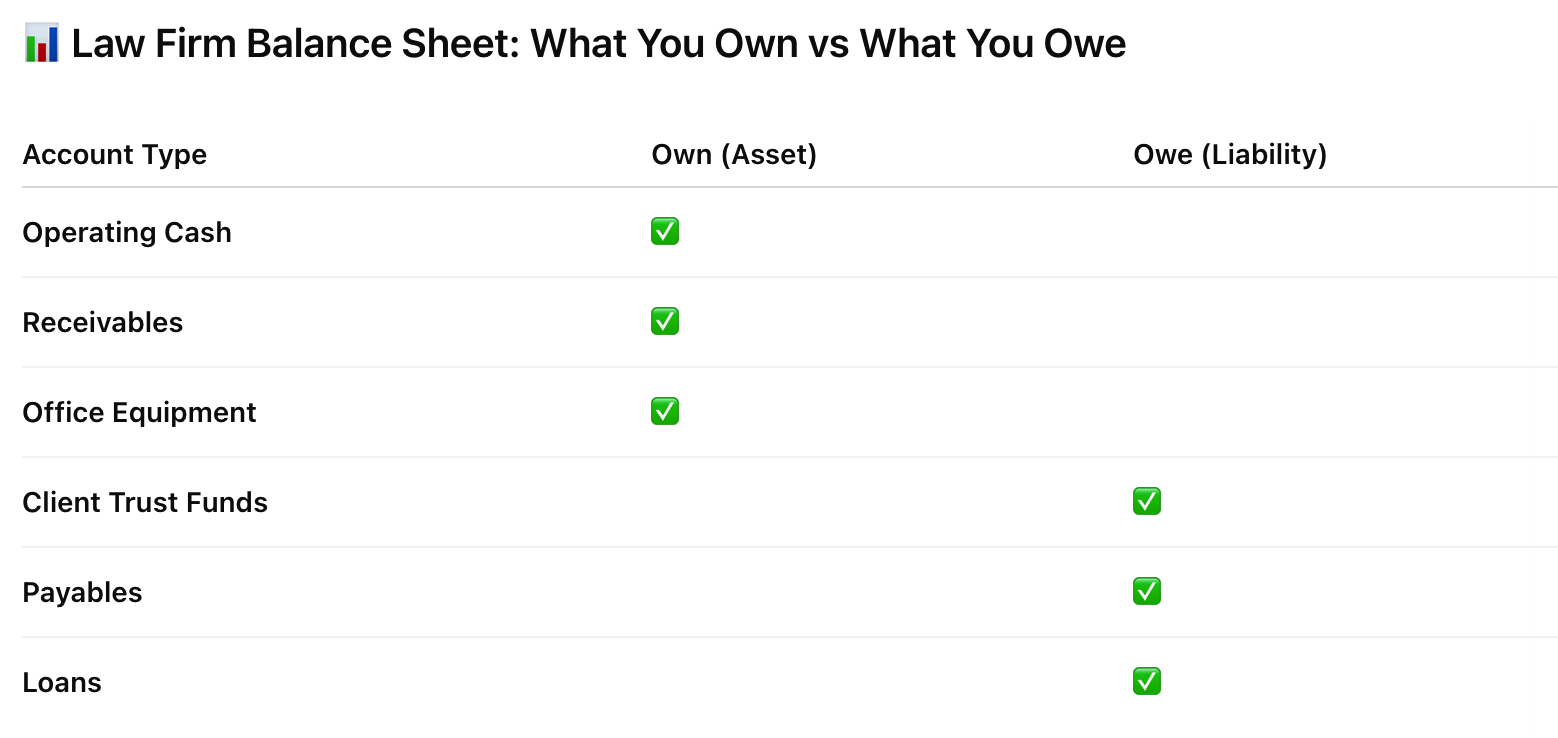

Law firms must classify operating cash, receivables, and office equipment as assets, while client trust funds, payables, and loans appear as liabilities on the balance sheet.

Learn more about maintaining accurate trust account balances through monthly three-way reconciliations.

Looking at both sides of the balance sheet helps you keep tabs on liquidity and keep firm and client money well apart. For firms, IOLTA accounts are always liabilities—those dollars are the client’s, not the firm’s. If you want to dig deeper, here’s a resource on trust account liabilities.

4. Commingling Trust and Operating Funds

The Mistake

Depositing client retainers into your operating account, leaving earned fees in trust "until you need them," or using trust funds to cover a short-term firm expense with intent to "replace it tomorrow."

Why It's a Violation

Client funds and firm funds must remain completely separate. Commingling violates every state's professional conduct rules. The bar doesn't care about your intent - only that it happened.

Real Example

Attorney deposits retainer check into operating account by mistake. Realizes error next day and transfers money to trust. Client complains about unrelated matter. Bar reviews records during investigation. Discovers commingling. Even though "no money was missing," attorney receives private reprimand.

How to Fix It

Client funds go in trust. Firm funds go in operating. No exceptions. If you make a deposit error, document the correction immediately with an explanation memo in your files.

Prevention

Use separate bank accounts with completely different account numbers. Never give yourself access to move money between trust and operating without a secondary review process.

Even small bookkeeping mistakes - like incomplete ledgers or skipped reconciliations - can distort a law firm's cash flow reports and threaten IOLTA compliance.

Proper trust account management requires structured oversight, monthly reconciliations, and client ledger precision - not casual bookkeeping. Specialized law firm bookkeeping services, like Accounting Atelier, proactively close these gaps before they escalate into compliance violations.

5. Stale Trust Balances (90+ Days)

The Mistake

A matter closed six months ago, but $400 remains in the client's trust ledger. You keep meaning to return it but haven't gotten around to it. Or you have balances from clients you can't locate.

Why It's a Violation

Stale balances signal poor trust management. In some states, old balances must be escheated to the state. At minimum, they trigger questions during audits: why are you holding funds for closed matters?

Real Example

Firm accumulates small balances ($50-500) across dozens of closed matters. Total stale balance exceeds $12,000. Bar audit identifies this as "improper retention of client funds." Firm required to attempt client contact, return funds, and implement balance review procedures.

How to Fix It

Review client ledgers monthly. When a matter closes, immediately disburse or return remaining funds. If you can't locate a client, follow your state's escheatment procedures.

Prevention

Add "trust balance review" to your case closing checklist. Don't mark a matter fully closed until trust balance is zero. Flag any balance over 90 days for immediate action.

6. Payment Processing Fee Errors

The Mistake

Client pays $3,000 retainer by credit card. Processor takes $90 fee, so $2,910 hits your trust account. You record $3,000 in the client ledger. Now your ledger shows $90 more than you actually have.

Why It's a Violation

Your client ledgers must match your bank balance exactly. Recording amounts you don't actually have creates false trust balances and reconciliation discrepancies.

Real Example

Firm accepts credit card payments for retainers. Records full amounts in client ledgers but doesn't account for processing fees. Three-way reconciliation doesn't balance. Takes firm two months to identify and correct issue. Meanwhile, trust account appears non-compliant.

How to Fix It

Record what actually hits the trust account, not what the client paid. If $2,910 hits trust, record $2,910 in the client ledger. Either absorb processing fees as a firm expense or clearly disclose them and charge them separately.

Prevention

Use payment processors designed for IOLTA compliance (like LawPay) that separate processing fees automatically. Review your state's ethics rules on passing processing fees to clients.

7. No Three-Way Reconciliation

The Mistake

You reconcile your trust bank statement to your books monthly—but you never verify that your client ledgers match. You assume if the bank reconciles, everything is fine.

Why It's a Violation

Bank reconciliation only proves your bank agrees with your records. It doesn't prove every dollar is properly allocated to a specific client. Three-way reconciliation (bank, trust ledger, client ledgers) is the bar's standard for compliance.

Real Example

Attorney reconciles bank account religiously. Feels confident in trust accounting. Bar audit requests three-way reconciliation report. Attorney discovers client ledgers are $6,000 off from actual bank balance. Cannot explain discrepancy. Violation cited.

How to Fix It

Monthly reconciliation must include three steps:

Reconcile bank statement to trust ledger (normal bank rec)

Sum all individual client ledger balances

Verify that sum equals both bank balance and trust ledger

All three must match exactly.

Prevention

Use software that generates three-way reconciliation reports automatically. Don't consider your trust reconciliation complete until all three numbers match.

For best practices, the American Bar Association provides a detailed trust accounting checklist to help firms uphold proper IOLTA requirements.

Critical trust accounting reports like three-way reconciliations and audit trails require precision. DIY bookkeeping often falls short, exposing law firms to compliance risks.

8. Missing Client Ledger Documentation

The Mistake

You track client funds in your head or in informal notes. You know roughly what each client has in trust but can't produce a detailed ledger showing every deposit, disbursement, and balance.

Why It's a Violation

Bar rules require detailed client ledgers showing every transaction. "I know what they have" isn't documentation. During audits, you must produce ledgers on demand.

Real Example

Solo practitioner maintains trust account but doesn't keep client-specific ledgers. Tracks balances in spreadsheet. Bar audit requests ledgers. Attorney cannot produce transaction-level detail. Cited for inadequate record-keeping despite no missing funds.

How to Fix It

Every client with funds in trust needs an individual ledger showing:

Date of each transaction

Description (deposit, disbursement, purpose)

Amount

Running balance

This isn't optional.

Prevention

Use practice management software (Clio, MyCase, LeanLaw) that automatically maintains client ledgers. Never rely on memory or informal tracking. For a complete breakdown of documentation requirements, see our guide to IOLTA recordkeeping requirements.

9. Improper Trust Account Titling

The Mistake

Your trust account is titled "Smith Law Firm" or "Attorney Operating Account" instead of clearly indicating it's a trust or IOLTA account.

Why It's a Violation

Trust accounts must be clearly identifiable as trust accounts. Proper titling protects against accidental misuse and signals compliance to banks and auditors.

Real Example

Firm opens "business checking" account to hold client funds. Doesn't realize it should be titled as IOLTA account. Bank doesn't report IOLTA interest to state program. Bar audit identifies improper account structure. Firm required to open properly titled account and transfer funds.

How to Fix It

Your trust account should be titled: "[Firm Name] IOLTA Account" or "[Firm Name] Client Trust Account." Verify your state bar's specific requirements.

Prevention

When opening a trust account, work with banks experienced in serving law firms. Confirm proper titling and IOLTA designation before making the first deposit.

10. Trust Ledger Recording Errors

The Mistake

You record a $5,000 deposit as $500. You record a disbursement to the wrong client. You forget to record a transaction entirely. Your trust ledger doesn't match reality.

Why It's a Violation

If your ledger is wrong, your reconciliation is wrong. You can't prove compliance if your records are inaccurate. Even innocent data entry errors are violations if they create discrepancies.

Real Example

Bookkeeper transposes numbers: records $1,500 as $15,000. Error goes unnoticed for three months. During reconciliation, discovers $13,500 discrepancy. Takes weeks to identify source. Trust account appears non-compliant during that period.

How to Fix It

Implement controls: require receipts for every transaction, review entries weekly, and catch errors fast. Correct mistakes immediately with clear documentation explaining the error and correction.

Prevention

Use bank feeds to auto-import transactions when possible. Review trust transactions weekly, not just monthly. Assign someone detail-oriented to trust accounting - accuracy matters more than speed.

What to Do If You've Made These Mistakes

If You Discover Errors Yourself

Don't panic. Fix it immediately:

Document what happened - Write a memo explaining the error, when it occurred, and how it happened

Correct the error - Transfer funds where they belong, update ledgers, fix balances

Document the correction - Note what you did to fix it and when

Implement prevention - Change your process so it doesn't happen again

Consider disclosure - In some jurisdictions, self-reporting minor errors demonstrates good faith (consult ethics counsel)

Most bars distinguish between patterns of negligence and isolated mistakes that are promptly corrected.

If You Receive a Bar Inquiry

Take it seriously. Respond promptly:

Don't ignore it - Missing deadlines makes everything worse

Gather documentation - Bank statements, reconciliations, client ledgers, everything requested

Be honest - Don't minimize or hide problems

Show correction - Demonstrate you've fixed the issue and implemented controls

Get help - Consider consulting a legal ethics attorney or professional liability counsel

For complex trust accounting issues, see our trust account cleanup service.

How to Prevent IOLTA Violations

Monthly Reconciliation (Non-Negotiable)

Complete three-way reconciliation by the 10th of every month. Match bank statement, trust ledger, and sum of client ledgers. All must equal exactly.

Client Ledger Review

Don't just sum the balances - review each ledger. Look for:

Negative balances (immediate red flag)

Stale balances (closed matters with funds remaining)

Unusually large balances (verify accuracy)

Separation of Duties

One person shouldn't handle all trust accounting without oversight. Have someone else review reconciliations monthly—partner, co-counsel, or outside bookkeeper.

Use Legal-Specific Software

Practice management systems designed for law firms (Clio, MyCase, LeanLaw) include trust accounting features and compliance controls. Generic accounting software often lacks necessary safeguards.

Professional Bookkeeping

Consider outsourcing trust accounting to a bookkeeper who specializes in law firms. The cost ($500-1,000/month) is far less than the consequences of violations.

Learn more about our law firm bookkeeping services.

Protect Your License: Get IOLTA Compliance Right

IOLTA mistakes aren't just bookkeeping errors—they're ethical violations that can derail your career. The good news: most violations are preventable with proper systems and monthly attention.

If your trust accounting isn't where it should be, fix it now. Monthly reconciliation, accurate client ledgers, and proper fund timing aren't complicated - they just require discipline and the right systems.

We specialize in IOLTA compliance and trust accounting for law firms. If you need help cleaning up trust accounts, implementing proper systems, or maintaining monthly compliance, we can help.

Frequently Asked Questions

-

Consequences depend on severity, pattern, and your response. Minor isolated errors corrected promptly might result in no action or required training. Repeated violations, failure to correct, or evidence of misappropriation can lead to suspension or disbarment. Most violations fall somewhere in between - resulting in private or public reprimands, required remediation, and monitoring.

-

Your IOLTA account is compliant if: (1) you complete monthly three-way reconciliation, (2) all three numbers match exactly, (3) no client ledgers show negative balances, (4) you can produce detailed client ledgers on demand, (5) fund transfers match actual work completion, and (6) you have no stale balances over 90 days. If any of these aren't true, you have compliance issues.

-

It depends on your jurisdiction and the nature of the error. Some states view self-reporting favorably. Others have no formal self-reporting mechanism. For significant violations, consult an ethics attorney before deciding. For minor errors (data entry mistakes, briefly negative ledgers immediately corrected), focus on fixing and documenting the correction.

-

You can and should fix errors regardless of when they occurred. Correct the accounting, document what you did, and implement better controls. If errors are substantial or span long periods, consider consulting an ethics attorney about how to handle disclosure and whether professional help is needed.

-

Random audits are relatively rare - most bars lack resources for broad auditing. However, targeted audits happen when: (1) client complaints trigger investigation, (2) you report issues yourself, (3) you're involved in disciplinary proceedings for other matters, or (4) you're selected in random compliance checks. Don't count on avoiding audits - count on being audit-ready.

-

IOLTA violations specifically involve pooled trust accounts used for retainers and short-term client funds. Trust accounting violations broadly include any mishandling of client funds - whether in IOLTA accounts, separate client trust accounts, or escrow accounts. All IOLTA violations are trust accounting violations, but not all trust accounting violations involve IOLTA accounts.

About the Author Written by Amy Coats, founder of Accounting Atelier. With over 20 years in financial management, Amy specializes in law firm bookkeeping and IOLTA compliance. She is a QuickBooks Online ProAdvisor, Clio Certified Consultant, and MyCase Partner - dedicated to helping solo attorneys and small firms build financially sound practices.