IOLTA Account: The Complete Guide for Law Firms

An IOLTA account (Interest on Lawyers' Trust Account) is a pooled trust account where attorneys hold client funds that are too small or too short-term to earn interest individually. The interest goes to state bar associations to fund legal aid. Every state requires lawyers to use an IOLTA when holding client funds, but the rules vary: California requires monthly written reconciliation, Texas mandates the State Bar's tax ID on the account, New York calls the program IOLA. Attorneys are responsible for IOLTA compliance even when a bookkeeper handles the records. This guide covers how IOLTA actually works on a monthly basis from the perspective of the bookkeeper who reconciles these accounts for solo and small law firms.

I've reconciled hundreds of IOLTA accounts over the past decade. Most compliance failures aren't intentional misconduct. They're attorneys who were never taught trust accounting in law school, handed a checkbook, and expected to figure it out. This guide covers what bar associations assume you already know.

IOLTA is one piece of the bigger picture. For the full framework see our guide to trust accounting for law firms.

What Does IOLTA Stand For?

IOLTA stands for Interest on Lawyer Trust Accounts (sometimes called Interest on Lawyers' Trust Accounts). The acronym varies by jurisdiction. New York uses IOLA (Interest on Lawyer Accounts) - but the underlying concept is consistent nationwide.

The "interest" component distinguishes IOLTA accounts from traditional client trust accounts. Before IOLTA programs emerged in the 1980s, small client deposits sat in non-interest-bearing accounts because the administrative cost of setting up individual interest-bearing accounts exceeded any potential earnings. State bars recognized an opportunity: pool these small amounts, generate meaningful interest collectively, and direct those earnings toward expanding access to justice.

Today, IOLTA programs in all 50 states fund legal aid organizations, pro bono programs, and civil legal services for low-income individuals. According to the American Bar Association, IOLTA programs have generated over $4 billion since 1981, with annual grants exceeding $175 million nationwide. The first IOLTA program launched in Florida in 1981; the ABA endorsed IOLTA in Formal Opinion 348 (1982). All 50 states now operate IOLTA programs.

How IOLTA Accounts Work

The mechanics operate on a straightforward principle with complex execution.

The Interest Flow

When you deposit client funds into your IOLTA account, the bank treats the pooled balance as a single interest-bearing account. Each month, the bank calculates interest on the total balance - not individual client portions - and remits that interest directly to your state's IOLTA program. You never touch the interest. Your clients never receive it. The bank handles the transfer automatically.

Example: Your IOLTA account maintains an average monthly balance of $50,000. The bank pays 0.5% APY. Approximately $20.83 in interest flows to your state IOLTA program that month. Scale that across thousands of attorneys statewide, and these nominal amounts fund millions of dollars in legal aid annually.

The Principal Protection

While interest leaves the account, every dollar of principal belongs to your clients—and you're personally responsible for safeguarding it. This fiduciary obligation means you must:

Know exactly how much belongs to each client at all times

Never commingle client funds with operating funds

Never use one client's funds to cover another client's matter

Disburse funds only when earned or when the client directs

The bank sees one account balance. Your records must track dozens or hundreds of individual client balances within that single account. This dual-ledger requirement creates the reconciliation complexity that trips up firms.

Eligible vs. Ineligible Funds

Not all client funds belong in IOLTA. The determining factors are amount and duration:

IOLTA-eligible: Funds too small or held too briefly to generate net interest for the client after accounting for bank fees and administrative costs

Non-IOLTA trust: Larger amounts held longer, where the client benefits from individual interest earnings

Most states set no specific dollar threshold, leaving the determination to attorney judgment. Here's how it works in practice:

A $3,000 retainer for a family law matter expected to last 60 days → IOLTA

A $5,000 flat fee for estate planning work billed over 90 days → IOLTA

A $75,000 personal injury settlement held pending medical lien resolution over 4-6 months → Individual client trust account

A $150,000 real estate escrow deposit held for 30 days → Individual account given the amount

The threshold I use with clients: amounts under $10,000 held for under 90 days go to IOLTA. Above those thresholds, evaluate whether the client would net more than the administrative costs of a separate account.

How Does Money Actually Move Through an IOLTA Account?

Here's the worked example I use with new law firm clients.

Client signs retainer. Client A signs a retainer agreement and pays a $7,500 retainer for litigation work.

Deposit to IOLTA. The $7,500 goes into the firm's IOLTA account because it has not been earned. Retainer is a liability, not income.

Work begins. A week later, the attorney works 6 hours on Client A's case at $350/hour, totaling $2,100 in earned fees.

Invoice generated. Client A receives an invoice showing $2,100 due from the retainer.

Client approval. Most state rules require client approval (or contractual authorization) before earned fees transfer out of trust.

Transfer to operating. Once approved, $2,100 transfers from IOLTA to the firm's operating account. The transfer is recorded in both the trust ledger and the operating ledger.

Balance remains. $5,400 remains in trust. The client ledger shows the new balance.

Reconciliation at month-end. Bank statement, trust ledger, and individual client balance all show $5,400.

If any of these eight steps gets recorded wrong (date, amount, ledger, matter number) the books are out of compliance. Three-way reconciliation is what catches it before the bar does. See Three-Way Reconciliation for Law Firms for the full mechanics.

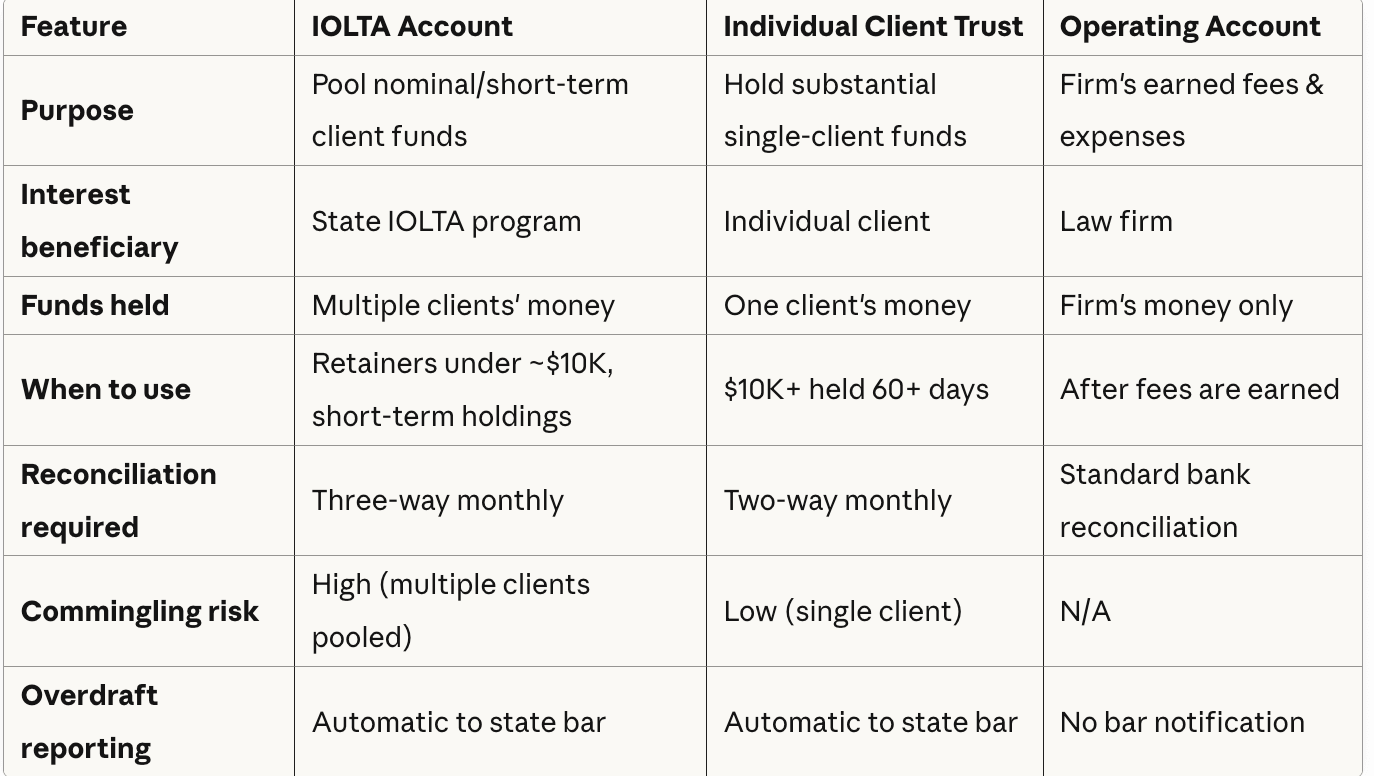

How Is an IOLTA Different From Other Trust Accounts?

Attorneys confuse IOLTAs with other trust structures all the time. The differences matter for compliance.

IOLTA vs. IOLA

New York calls its program IOLA (Interest on Lawyer Account). Same structure, different terminology. The IOLA Fund administers the program. If you practice in New York, you'll see "IOLA" in the rules; everywhere else, "IOLTA."

IOLTA vs. Individual Attorney Trust Account

An IOLTA holds pooled small or short-term funds; interest goes to state bar legal aid programs. An individual attorney trust account holds substantial or long-term funds for one client; interest goes to that client. The difference is who keeps the interest.

The threshold I use with clients: amounts under $10,000 held for under 90 days go to IOLTA. Above those thresholds, evaluate whether the client would net more than the administrative costs of a separate account.

IOLTA vs. Client Trust Account

All IOLTAs are client trust accounts. Not all client trust accounts are IOLTAs. "Client trust account" is the general category. IOLTA is the specific type used when funds are pooled and the bank remits interest to the state bar program.

IOLTA vs. Escrow Account

Escrow accounts hold funds neutrally during a transaction (real estate closings, settlement disbursements). Interest distribution is governed by the escrow agreement. IOLTA is specifically for client funds held by an attorney during legal representation. A title company's escrow account is not an IOLTA. An attorney holding earnest money for a real estate transaction uses their IOLTA.

Who Needs an IOLTA Account

If you're a licensed attorney who holds client funds - even occasionally - you need an IOLTA account. This includes:

Solo practitioners handling retainers, settlements, or real estate closings

Law firms of any size with client-facing billing

Of counsel attorneys who receive funds independently

Contract attorneys who handle client funds directly

The only attorneys exempt from IOLTA requirements are those who never hold client money. If your practice involves flat fees paid entirely upfront as earned, or if you work exclusively as in-house counsel, you don't need an IOLTA account. Everyone else does.

Establish your IOLTA account before you need it. Opening an account takes weeks. A client handing you a settlement check requires immediate deposit.

How to Open an IOLTA Account

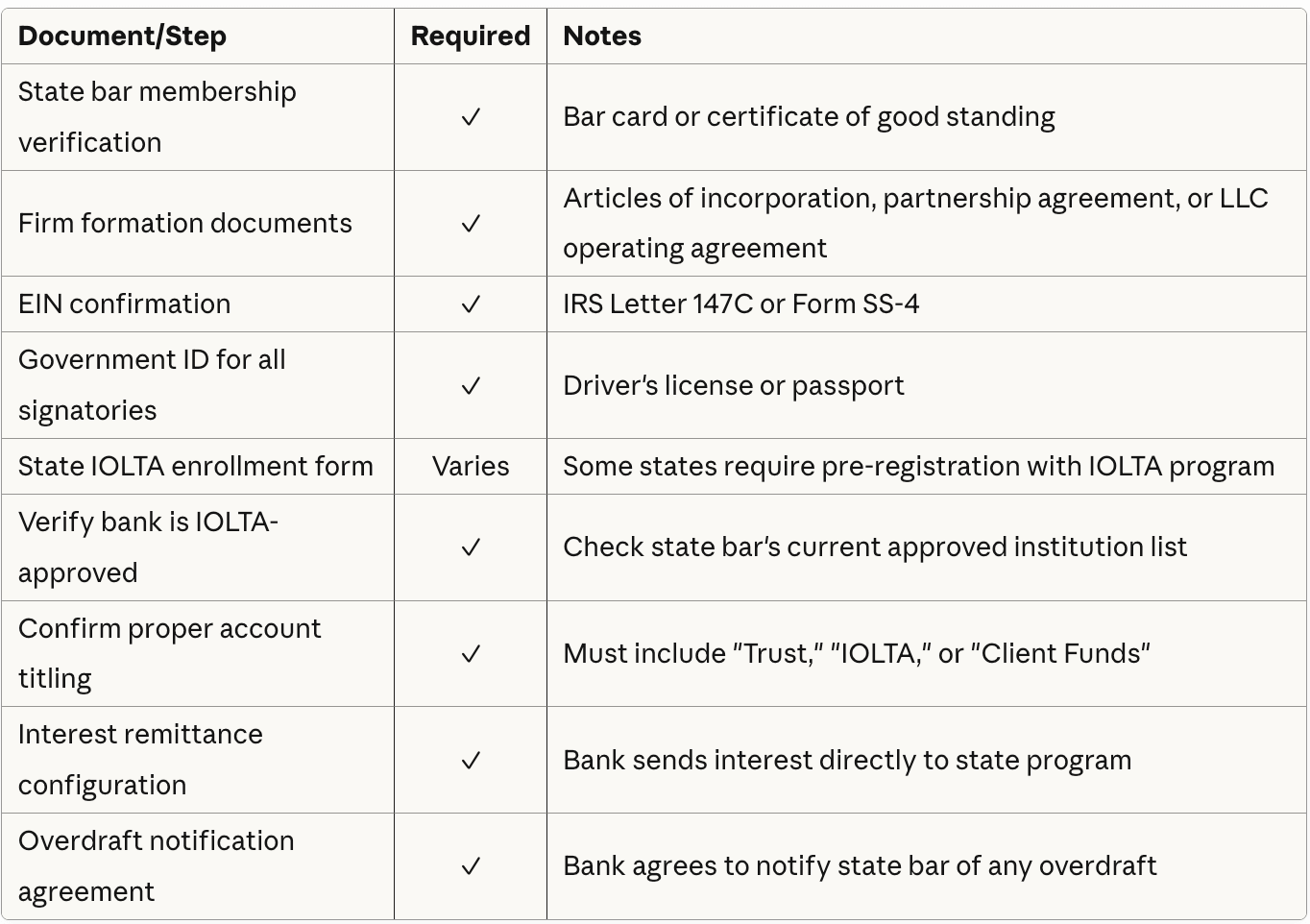

Opening an IOLTA account requires more documentation than a standard business account.

Step 1: Verify Your State Bar Requirements

Before visiting any bank, check your state bar's IOLTA program website for:

Approved financial institutions (not all banks participate)

Required account titling format

Reporting obligations

Minimum interest rate requirements (some states mandate rates)

Your state bar maintains a list of IOLTA-approved banks. Using a non-approved institution creates compliance issues regardless of how well you manage the account. The National Association of IOLTA Programs (NAIP) maintains links to every state program.

Step 2: Gather Required Documentation

Step 3: Select a Participating Bank

Choose a bank that participates in your state's IOLTA program. Evaluate:

Interest rates paid to the IOLTA program (higher rates mean greater legal aid funding)

Fee structures (some banks waive fees on IOLTA accounts)

Online banking capabilities for reconciliation

Check imaging and transaction detail access

Branch accessibility if you handle cash or physical checks

Step 4: Open the Account with Proper Titling

Your IOLTA account title must clearly identify it as a trust account. Standard formats:

[Firm Name] IOLTA Trust Account [Firm Name] Attorney Trust Account - IOLTA [Attorney Name], Esq., IOLTA Account

The bank will configure the account to remit interest directly to your state IOLTA program and provide the program with periodic balance reports. You'll receive monthly statements showing all transactions but no interest credits (interest transfers automatically to the state program).

Step 5: Establish Your Recordkeeping System

Before depositing a single dollar, establish your client ledger system. Track:

Individual client balances within the pooled account

Source and purpose of each deposit

Recipient and authorization for each disbursement

Running reconciliation between bank balance and total client ledgers

Whether you use legal practice management software, accounting software with sub-ledger capabilities, or manual ledger cards, your system must maintain the integrity of these records indefinitely. Most state bars require trust account records be retained for five to seven years after matter closure.

Step 6: Register with Your State IOLTA Program

Most states require attorneys to register their IOLTA accounts directly with the state program:

Account number and bank name

Attorney bar number

Firm contact information

Some states handle registration through annual bar dues or licensing renewals. Verify your state's process.

IOLTA Compliance Overview

IOLTA compliance extends beyond opening the right type of account. Ongoing obligations vary by state but generally include:

Record Retention Requirements

Maintain complete trust account records:

Bank statements and reconciliations

Client ledger cards or software records

Deposit slips and supporting documentation

Disbursement records with client authorizations

Three-way reconciliation reports

Overdraft Notification

Most states require banks to notify the state bar of any trust account overdraft - even a $1 shortage lasting one day. This automatic reporting means innocent errors trigger bar inquiry. Proper reconciliation prevents these situations.

Audit Readiness

State bars conduct random and for-cause trust account audits. Your records must demonstrate compliance on demand - systematic documentation, not reconstruction from memory.

For a comprehensive breakdown of compliance requirements and implementation, see our guide to IOLTA compliance requirements.

Monthly IOLTA Management Routine

Attorneys who avoid compliance issues follow structured routines that catch discrepancies before they become problems.

Daily Monitoring

Review your trust account balance and recent transactions daily. Five minutes. You're looking for:

Unexpected debits or fees

Returned deposits or failed transactions

Balance anomalies indicating errors

Weekly Reconciliation

Reconcile your bank balance against your total client ledgers weekly. The figures must match. Any discrepancy requires immediate investigation - not next month, not when you have time.

Monthly Three-Way Reconciliation

The cornerstone of trust accounting is the three-way reconciliation: your adjusted bank balance, your trust account ledger, and the sum of all individual client ledgers must equal the same figure. This triangulated verification catches errors that simple bank reconciliation misses.

A firm handling 30 active client matters:

Bank statement balance: $47,250.00

Less outstanding checks: ($2,100.00)

Adjusted bank balance: $45,150.00

Trust ledger balance: $45,150.00

Sum of 30 client ledgers: $45,150.00

All three figures match. If they don't, you have an error requiring identification and correction before closing the month.

Quarterly Review

Review dormant balances quarterly. Funds sitting untouched for 90+ days indicate:

Matters that closed without final disbursement

Client overpayments requiring refund

Unclaimed funds requiring escheatment evaluation

Address these balances proactively.

What Does a Legal Bookkeeper Catch That Attorneys Miss?

The IOLTA That Balanced But Wasn't Right

A firm came to me convinced their IOLTA was clean because the bank reconciliation matched every month. The bank balance and the trust ledger total agreed. The third leg of the reconciliation, the sum of individual client ledgers, was off by $47,000. Two clients had been overcredited; three had been undercredited. The bar wouldn't have cared that the bank reconciled. They would have cared that client funds weren't where the records said they were.

The Mixed-Purpose Check Deposited Wrong

An attorney took a $4,200 check from a new client. $1,200 was for filing fees and costs (client funds, belong in trust). $3,000 was a flat fee already earned (firm income, belongs in operating). She deposited the whole check into operating because that's where her bookkeeper had set things up. The fix: redeposit the trust portion to IOLTA, document the correction, and reset the firm's intake process so the next mixed-purpose check goes to IOLTA first.

The 18-Month Retainer

A retainer aged 18 months in a firm's IOLTA. The work had been done. The fees had been earned. The transfer from trust to operating had never happened. The attorney had forgotten about it; the bookkeeper didn't know to flag it. Stale balances in trust look fine on a reconciliation but the bar reads them as commingling.

The Bank Fee That Shouldn't Be There

Most IOLTA-friendly banks waive fees on these accounts. Some don't. When fees hit IOLTA, they should be reimbursed from operating immediately, with documentation. I've seen firms let monthly fees accumulate against a tiny "buffer" balance the attorney deposited. That buffer is the attorney's money sitting in a client trust account. Commingling.

The Wrong Matter Number

A trust deposit got recorded against the wrong matter number. The bank balance reconciled. The trust ledger reconciled. The two affected client ledgers were each off by the same amount in opposite directions. Looks fine in aggregate. Hidden completely until you reconcile the third leg, the sum of individual client ledgers, against the trust ledger total.

Three-way reconciliation catches all five of these. Two-way reconciliation catches none of them.

Common IOLTA Mistakes

Trust account violations account for a significant percentage of attorney discipline cases. Most stem from avoidable administrative errors rather than intentional misconduct.

The mistakes I encounter most frequently when onboarding new law firm bookkeeping clients:

Commingling earned fees with client funds — leaving earned fees in trust too long. You bill $1,200 against a client's $5,000 retainer on March 15. By April 30, that $1,200 should have moved to your operating account. Leaving it in trust beyond a reasonable billing cycle creates commingling.

Disbursing before deposits clear — treating deposited checks as immediately available. A client's $8,500 settlement check deposited Monday isn't available until it clears (2-5 business days). Disbursing against it Tuesday risks overdraft if the check bounces.

Inadequate client ledger maintenance — relying on memory or bank statements alone without tracking individual client balances within the pooled account.

Failing to reconcile monthly — discovering errors months after they occurred, making correction exponentially harder.

Improper check signing practices — pre-signed checks, single-signatory on large disbursements, or allowing non-attorney staff to sign without proper controls.

For a detailed examination of trust accounting errors and prevention, see our guide on common IOLTA mistakes.

How Do IOLTA Rules Differ by State?

Core IOLTA principles apply nationally. Implementation varies. Here's what changes in the seven states that send the most search traffic to this page.

Requirements change. Verify current rules with your state bar's IOLTA program.

California

Monthly written reconciliation required

Records held 5 years past representation end

Use State Bar-approved banks (current list available at the State Bar of California website)

IOLTA Notice to Financial Institution required

California requires interest rates comparable to non-IOLTA accounts at the same institution

See California IOLTA Trust Account Rules for the full breakdown.

New York

Called IOLA (Interest on Lawyer Account)

Bookkeeping records required under Rule 1.15(d)

Biennial attorney registration includes trust account information

IOLA Fund administers the program

Texas

State Bar's tax ID required on the account: 74-2354575 (Texas Access to Justice Foundation)

IOLTA Notice to Financial Institution form required within 30 days

Must use approved institutions

Detailed retention rules

Florida

Monthly three-way reconciliation required

6-year retention for trust records

Specific reconciliation report format

Random audits by The Florida Bar

Banks must pay at least 75% of the federal funds target rate

Illinois

IOLTA program operating since 1983

Lawyers Trust Fund of Illinois administers the program

Annual compliance certification required

Michigan

Michigan State Bar Foundation administers the IOLTA program

Comparable interest rate requirement on IOLTA accounts

Trust account records held minimum 5 years

Specific approved financial institution list

Arizona

Arizona Foundation for Legal Services & Education administers the program

Rule 1.15 of the Arizona Rules of Professional Conduct governs trust accounts

Trust account records held minimum 5 years

Annual compliance reporting required

Multi-Jurisdictional Practice

Each state's requirements apply to funds related to matters in that state. A California attorney handling a Texas matter must comply with Texas trust account rules for those funds. Some states permit out-of-state IOLTA accounts for attorneys primarily practicing elsewhere; others require in-state accounts for any matters involving their jurisdiction.

Common solution: maintain your primary IOLTA in your home state, open jurisdiction-specific accounts only when required by rule.

If your state isn't covered above, see Attorney Trust Account Rules: A State-by-State Guide for the full state-by-state breakdown.

What Software Do Law Firms Use to Manage IOLTA Accounts?

Practice management software with built-in trust accounting handles most of the IOLTA mechanics that QuickBooks alone cannot. The four most common platforms for solo and small firms:

Clio has the deepest practice management trust accounting feature set. Trust ledgers per matter, automated three-way reconciliation reports, IOLTA-compliant payment processing through Clio Payments. See our Clio Accounting Review.

MyCase offers simpler trust accounting suited for firms that want practice management without Clio's complexity. See our MyCase Accounting Review.

CosmoLex combines practice management, accounting, and trust in one system. The all-in-one approach reduces integration headaches. See our CosmoLex Review.

QuickBooks alone has no built-in IOLTA structure. You can configure it for trust accounting, but every safeguard has to be built manually. See our QuickBooks for Law Firms guide.

For a deeper feature comparison, see Best IOLTA Trust Accounting Software for Law Firms 2026.

Software does not replace a bookkeeper who knows how to read a three-way reconciliation. Your bookkeeper needs access to BOTH the practice management platform AND QuickBooks for trust compliance to work. The platform handles the trust ledger; QuickBooks handles the firm's books. The two have to reconcile.

At Accounting Atelier, we developed the Legal Ledger Protocol™ specifically for law firm trust accounting: a systematic approach to IOLTA management that integrates with your practice management software while maintaining the documentation rigor bar auditors expect.

Trust Accounting That Survives a Bar Audit

IOLTA compliance doesn't have to consume your practice. Proper systems, consistent routines, and clear documentation turn trust accounting into a manageable operational function.

If your IOLTA account needs cleanup, reconciliation, or systematic management, Accounting Atelier specializes exclusively in law firm bookkeeping - including trust accounting for firms with complex IOLTA requirements. We implement the Legal Ledger Protocol™ to bring your trust accounts into compliance and keep them there.

Schedule a trust account review →

Frequently Asked Questions

-

IOLTA accounts are checking accounts. The checking structure provides the liquidity attorneys need for frequent deposits and disbursements - savings account transaction limits don't work for client fund management. Banks classify IOLTA accounts as Negotiable Order of Withdrawal (NOW) accounts or Business Interest Checking, allowing interest to accrue while maintaining on-demand access.

-

Your bank notifies your state bar automatically. Even if the overdraft resulted from a bank error or timing issue, expect a letter from the bar requesting explanation. Document everything: the cause, your correction, steps taken to prevent recurrence. Most bars treat inadvertent, promptly-corrected overdrafts differently than patterns of mismanagement - but the inquiry process creates administrative burden regardless. I've seen attorneys receive bar inquiries over $12 overdrafts caused by unanticipated bank fees.

-

No. Interest flows to the state IOLTA program for legal aid funding - not to you or your clients. To earn interest on funds, hold them in a different account type: your operating account for earned fees, or an individual client trust account for substantial client funds.

-

Zero of your own money. IOLTA accounts contain only client funds. Some attorneys deposit a small amount ($50-100) to cover bank fees, but most states prohibit or strictly limit this practice. Check your state rules - many require banks to waive fees on IOLTA accounts or require fees be paid from your operating account.

-

Yes. Some firms benefit from separate accounts for different practice areas. A firm handling personal injury settlements and real estate closings might maintain separate IOLTA accounts for cleaner recordkeeping. Each account requires independent reconciliation and compliance monitoring. I work with one firm that maintains three IOLTA accounts: litigation, transactional, and real estate - each with its own three-way reconciliation.

-

Both hold funds belonging to others pending specific conditions. The distinction is regulatory: IOLTA accounts are specifically for attorney-held client funds under state bar rules, with interest directed to legal aid programs. "Escrow account" applies to real estate escrow, third-party escrow services, or other holding arrangements outside the attorney trust account framework. A title company's escrow account is not an IOLTA; an attorney holding earnest money for a real estate transaction uses their IOLTA.

-

Most states require retention for five to seven years after the matter closes or the attorney-client relationship ends. Some states require permanent retention. Given minimal storage costs for digital records, retain trust account records indefinitely - they surface in malpractice defense or client disputes long after formal retention periods expire.

-

Funds remaining after reasonable efforts to locate the client must be escheated to the state as unclaimed property. Timelines vary by state - typically one to five years holding plus documented good-faith contact efforts. Never keep unclaimed funds or transfer them to your operating account. Review balances over 12 months old quarterly to prevent accumulation.

-

State rules vary, but most permit authorized staff signatories with appropriate controls. Best practices: dual-signature requirements above $5,000, prohibition of pre-signed checks, regular review of all disbursements by an attorney. Delegation of signing authority doesn't delegate fiduciary responsibility - the attorney remains accountable for all trust account transactions.

-

You need trust accounts complying with rules governing each matter's jurisdiction. Some states permit out-of-state IOLTA accounts for attorneys primarily practicing elsewhere; others require in-state accounts for any matters involving their jurisdiction. Multi-jurisdictional practice requires careful analysis of each state's requirements. Common solution: maintain your primary IOLTA in your home state, open jurisdiction-specific accounts only when required by rule.

-

Credit card retainers present trust accounting challenges. The deposit posts to your merchant account (operating), but funds aren't earned yet (trust). Transfer retainer amounts from operating to trust immediately upon receipt, document the transfer, and maintain the client ledger in trust until fees are earned. The processing fee (2.5-3.5%) comes from operating funds, not the client's retainer. Client pays $5,000 retainer by credit card, fees are $150: you transfer $5,000 to trust and absorb the processing fee.