Clio and QuickBooks Integration for Law Firms: Trust Accounting Configuration

Last quarter, we inherited a QuickBooks file from a firm that had been running the Clio integration for eighteen months. The integration had been "working" - invoices synced, payments recorded, reports generated. But when we ran the three-way reconciliation, the trust liability account in QuickBooks showed $47,000 more than the sum of client balances in Clio. Eighteen months of trust payments had been crediting the wrong accounts, and no one caught it because the integration kept running without errors.

The Clio and QuickBooks integration connects your practice management system to your accounting software, syncing invoices, payments, and client data between the two platforms. It eliminates double-entry for operating transactions. But it does not handle trust accounting - and that gap is where configurations go wrong.

As a Clio Certified Partner, I have set up this integration for dozens of firms. The technical connection takes ten minutes. Getting it right for a firm that handles client funds takes actual thought.

How Do I Set Up Clio with QuickBooks Online for My Law Firm?

The connection starts in Clio Manage under Settings, then Bill Syncing. Click Connect next to QuickBooks Online, sign into your Intuit account, and authorize the connection. The technical link takes less than ten minutes. But the configuration decisions you make during setup determine whether this integration helps your practice or creates months of cleanup work.

Before connecting, your QuickBooks file needs a specific structure. Separate bank accounts for operating and IOLTA. A trust liability account with client-level sub-accounts if your state requires individual client ledgers (California, New York, Texas, and Florida all do). Income accounts that match your Clio billing categories, not a single "Legal Services" catch-all. If any of this is missing, fix it first. The integration syncs whatever exists, including the mess.

After connecting, four configuration decisions matter:

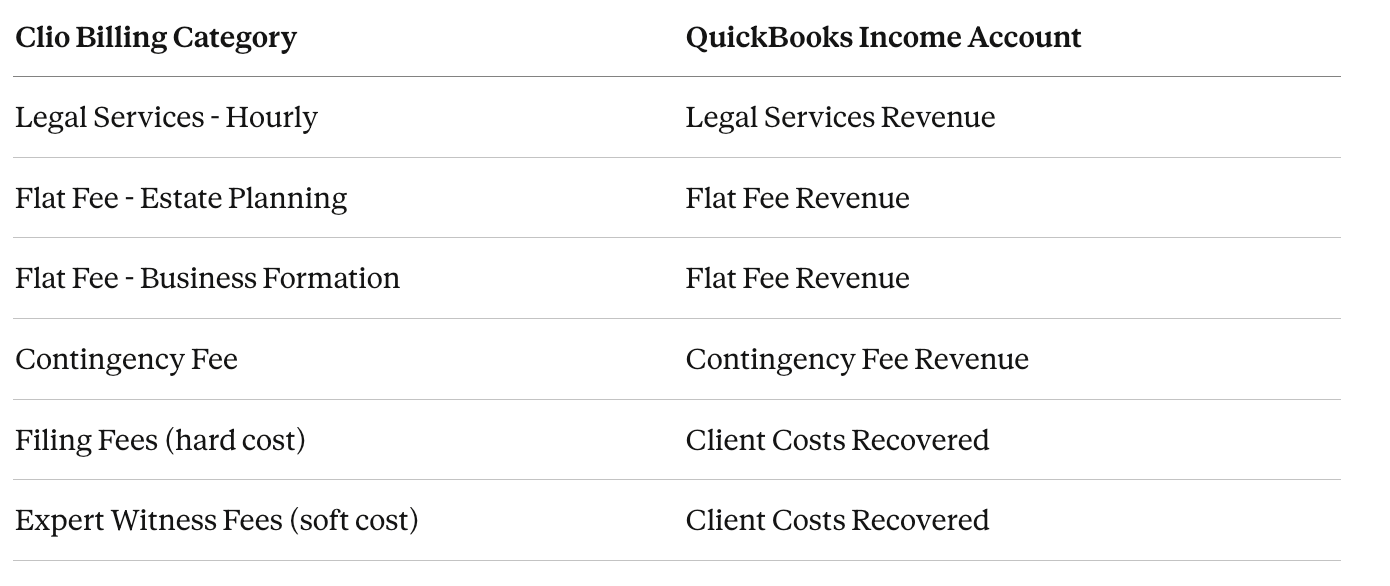

Map your Clio billing categories to the correct QuickBooks income accounts. Every category needs a destination. Create a mapping document before you start: Clio billing category in one column, QuickBooks income account in the other.

Set invoice sync timing to batch rather than real-time. Real-time sync pushes draft invoices to QuickBooks before they are finalized. Batch sync, timed to your invoicing cycle, sends only finished invoices.

Create separate payment methods in Clio for operating payments and trust applications. Map them to different workflows in QuickBooks. Operating payments go through standard accounts receivable. Trust applications trigger transfer entries. If these flow through the same path, your operating account will show cash that is not there.

Use bank feeds in QuickBooks only, not in both systems. Running dual bank feeds creates duplicate transactions that take hours to untangle. Let the integration create invoice and payment records in QuickBooks, then match them against bank feed transactions using QuickBooks' match function.

For firms using QuickBooks Online Plus or Advanced, the native Clio integration handles operating transaction sync at no additional cost. Clio requires QBO Essentials or higher for the integration, though Plus or Advanced gives you the class and project tracking most law firms need for matter-level reporting.

Why Clio Needs QuickBooks (and Vice Versa)

Clio tracks your practice. QuickBooks tracks your money. The confusion starts when people treat them as interchangeable.

Clio is where you record time, generate invoices, manage matters, store documents, and track what clients owe you. It also maintains client trust balances - the money sitting in your IOLTA account that belongs to clients, not to you. Clio does these things well.

What Clio cannot do: produce a balance sheet, track accounts payable, calculate your quarterly tax estimates, or give your CPA the financials they need at year-end. Clio knows your revenue and your trust balances. It does not know your rent, your payroll, your equipment loans, or your actual profit.

QuickBooks for law firms fills that gap. It holds your complete financial picture - assets, liabilities, equity, revenue, expenses. It reconciles to your bank. It produces the reports that tell you whether you're actually making money or just busy.

You need both. The integration connects them so you're not entering invoices twice. But the integration only handles the operating side. Every trust transaction still requires manual work in QuickBooks, and that's where most firms get into trouble.

Before You Connect: The Pre-Integration Audit

The integration syncs whatever mess exists. Connect it to a disorganized QuickBooks file and you'll have organized chaos - everything flowing smoothly into the wrong places.

I have seen firms connect the integration to QuickBooks files with seventeen different income accounts, half of them duplicates from years of ad-hoc additions. The sync worked perfectly. The reporting was useless. If your chart of accounts needs cleanup, do it before connecting. Our trust account cleanup process exists because so many firms skip this step.

Your QuickBooks file needs a specific structure before the integration makes sense. You need separate bank accounts for operating and IOLTA - obvious, but I have seen them combined. You need a trust liability account, and if your state requires client-level ledgers (California, New York, Texas, and Florida all do), you need sub-accounts under that liability for each client with funds on deposit. You need income accounts that actually match your Clio billing categories, not a single "Legal Services" catch-all that tells you nothing about your revenue mix.

On the Clio side, review your billing categories and payment allocation settings before enabling sync. Create a mapping document: Clio billing category in one column, corresponding QuickBooks income account in the other. Every category needs a destination.

Here's what a clean mapping looks like:

Avoid the "Legal Services" catch-all that tells you nothing about your revenue mix. Granular mapping takes ten extra minutes during setup and saves hours of reporting frustration later.

If you find Clio categories without clear QuickBooks matches, fix them first. The integration will ask for this mapping - fumbling through it during setup creates errors.

One decision matters more than people realize: bank feeds. Use QuickBooks bank feeds or Clio bank feeds, not both. Running dual bank feeds creates duplicate transactions that take hours to untangle. Most firms do better with bank feeds in QuickBooks only, letting the integration create invoice and payment records that match against those feeds.

Trust Accounting Configuration: Where Integrations Fail

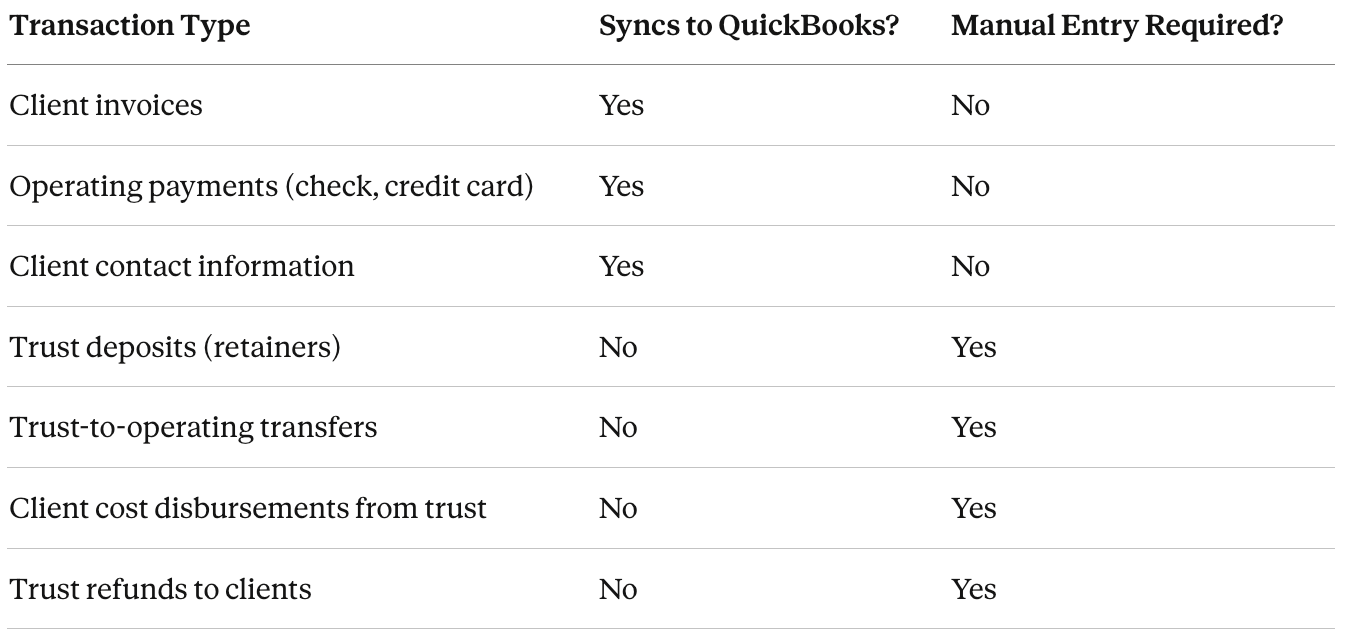

The Clio QuickBooks integration does not sync trust transactions. This is correct - trust accounting requires controls that prevent errors from propagating automatically. But the boundary between what syncs and what doesn't creates problems that show up months later during reconciliation.

Here's what the integration handles and what it ignores:

Every "No" in that middle column is a potential failure point.

Trust deposits allocated to the wrong client

When a retainer arrives, you record it in Clio as a trust deposit to that client's balance. In QuickBooks, the deposit hits your bank feed, and someone categorizes it to the trust liability account. If you use sub-accounts per client - and your bar almost certainly requires this - you have to select the correct client sub-account manually.

I have seen firms categorize every trust deposit to the parent liability account without client allocation. The total trust liability looked correct, so nobody questioned it. But the client-level detail was fiction, and when the firm faced a random bar audit, they had 47 client ledger discrepancies totaling $31,000 in misallocations. Every deposit for eight months had hit the parent account instead of the client sub-account. Reconstructing the correct allocation took weeks.

The fix is boring but necessary: a trust deposit workflow that requires client sub-account selection, every time, with the client name verified against the deposit slip before categorization.

Trust-to-operating transfers recorded as phantom revenue

When you apply trust funds to pay a client invoice in Clio, the integration sees a "paid" invoice and records a payment in QuickBooks. The default behavior credits your operating bank account and debits accounts receivable.

That's wrong. The money did not materialize from nothing. It transferred from your IOLTA account to your operating account. The correct QuickBooks entry has two parts: a bank transfer (debit operating, credit IOLTA) and a liability reduction (debit trust liability, credit accounts receivable). If your payment method mapping sends trust applications through the standard payment flow, your operating account shows cash that isn't there.

We onboarded a firm last year with $23,000 in phantom cash. Their QuickBooks operating balance was $23,000 higher than the actual bank balance because eighteen months of trust-to-operating transfers had been double-counting the cash. The integration was "working." The books were wrong.

The fix: create a separate payment method in Clio for trust applications, and map it to a transfer workflow in QuickBooks rather than a standard payment receipt.

Voided invoices leaving orphaned payments

Void an invoice in Clio after it has synced to QuickBooks and you've created a reconciliation puzzle. Sometimes the void syncs and reverses the QuickBooks invoice. Sometimes it doesn't, and you have an orphaned invoice in QuickBooks that Clio no longer knows about.

Both scenarios create problems if payments were involved. A voided invoice with a recorded payment leaves an unexplained credit balance in A/R. An orphaned invoice that someone manually deletes from QuickBooks—without voiding the associated payment - creates a reconciliation gap that surfaces during month-end close.

The fix: void in Clio first, verify the sync completed, then clean up payment artifacts in QuickBooks. Never delete invoices in QuickBooks that came from Clio. Void them so the audit trail survives.

Duplicate entries from parallel data entry

This happens constantly. A firm enables the integration on a QuickBooks file that already has manually-entered invoices. The integration creates new invoices for the same clients, doubling everything. Or staff enter a transaction in QuickBooks without realizing the sync will create it automatically.

One firm had three months of duplicate invoices before anyone noticed. Their P&L showed $180,000 in quarterly revenue. Actual revenue was $90,000.

The fix: before enabling integration, clear all open invoices in QuickBooks for clients managed in Clio. Going forward, one rule: invoices originate in Clio, period. Anyone working in QuickBooks needs to know this.

Bank feed conflicts with synced payments

With QuickBooks bank feeds active and the Clio integration running, the same deposit can appear twice - once from the bank feed, once from the synced payment. If someone categorizes the bank feed transaction without matching it to the synced record, you've double-booked the revenue.

The accounts might still reconcile to the bank. But your A/R aging shows mysterious credits, and your revenue-by-client reports are overstated. These errors hide until someone digs into the detail.

The fix: train anyone working in QuickBooks to use the "match" function for bank feed transactions that correspond to Clio payments. Match, don't categorize independently.

Does the Clio Integration Handle Trust Accounting in QuickBooks?

No. The Clio QuickBooks integration syncs operating transactions only. It does not sync trust deposits, trust-to-operating transfers, or client-level trust ledger entries. This is by design. Trust accounting requires controls that prevent errors from propagating automatically, and automated sync without those controls creates exactly the kind of discrepancies that trigger bar audits.

Every trust transaction in QuickBooks requires manual entry by someone who understands Rule 1.15 requirements. When a retainer arrives, you record it in Clio as a trust deposit to that client's balance. In QuickBooks, the deposit hits your bank feed, and your bookkeeper categorizes it to the correct client sub-account under trust liabilities. When trust funds are applied to pay an invoice, the correct QuickBooks entry has two parts: a bank transfer from IOLTA to operating, and a liability reduction from the client's trust sub-account. The integration handles neither of these.

Monthly three-way reconciliation is required regardless of the integration. Your bookkeeper reconciles the IOLTA bank statement balance, the trust ledger balance in QuickBooks, and the total of all individual client balances in Clio. All three must match. When they do not, the discrepancy must be identified and corrected before the books close. At Accounting Atelier, we perform this reconciliation as part of every law firm engagement.

Integration Settings That Actually Matter

Clio's documentation covers the click-by-click setup. What matters more: the configuration decisions that determine whether this integration helps you or creates cleanup work.

Invoice sync timing: Real-time sync sounds efficient. In practice, it causes problems. Save a draft invoice in Clio - maybe you're adding time entries throughout the day - and real-time sync pushes an incomplete invoice to QuickBooks. Now you have to edit it in both places or wait for the edit to sync and hope it overwrites cleanly.

Weekly batch sync, timed to your invoicing cycle, produces cleaner results. Finalize everything in Clio first, then let the batch run. Only finished invoices hit QuickBooks.

Payment method mapping: This is where trust accounting lives or dies. Create distinct payment methods in Clio for operating payments (checks, credit cards, ACH) and trust applications. Map them to different workflows in QuickBooks. Operating payments go through standard accounts receivable. Trust applications trigger transfer entries. Do not let them flow through the same path.

Contact sync direction: Clio-to-QuickBooks, one way. Clio is your system of record for client information. Bidirectional sync creates duplicates when someone edits a contact in both systems. One-way sync, Clio as source, eliminates the conflict.

Expense sync: Skip it. The integration can push Clio expenses to QuickBooks, but they arrive without the categorization detail QuickBooks needs. You end up re-categorizing everything anyway. Enter expenses directly in QuickBooks or let them flow through bank feeds. Use Clio for matter-level cost tracking, QuickBooks for firm-level expense management.

When the integration breaks: It will. Authorization tokens expire, API updates cause temporary failures, syncs fail silently. Build verification into your workflow: weekly invoice count comparison between systems, monthly sync log review in Clio settings, immediate investigation of any error notifications. When the connection drops, re-authorize it and manually verify every transaction that crossed the outage. Do not assume the sync catches up automatically.

LeanLaw vs. Native Integration

Some firms use LeanLaw as middleware between Clio and QuickBooks instead of the native integration. LeanLaw costs money (the native integration is free), so the question is whether the additional features justify the expense.

My take: for most firms with straightforward billing and a single IOLTA account, the native integration works fine if you configure it correctly and maintain the manual trust workflows. The failure modes above aren't integration failures - they're configuration and process failures. The native integration can work.

LeanLaw makes sense in specific situations: firms with multiple trust accounts that need consolidated reporting, firms with LEDES billing requirements, firms where the trust volume is high enough that manual QuickBooks entries become a real time burden. LeanLaw's trust accounting features are genuinely better than the native integration's approach of "just don't sync trust at all."

If you're debating between them: start with the native integration, implement proper trust workflows, and evaluate after six months. If the manual trust entries are eating significant time or creating errors despite good processes, LeanLaw may be worth the cost. If things are running smoothly, you don't need it.

What Should I Look for in a Bookkeeper Who Handles Clio and QuickBooks?

Not every bookkeeper who works in QuickBooks understands the Clio integration, and not every bookkeeper who uses Clio understands trust accounting. You need someone who knows all three.

Ask whether they are a Clio Certified Partner. Ask whether they are a QuickBooks Online ProAdvisor. Ask how they handle trust transactions that the integration does not sync. Ask about their three-way reconciliation process. If they describe reconciling only the bank statement to the QuickBooks ledger without mentioning Clio client balances as the third number, they are not performing trust-compliant bookkeeping.

At Accounting Atelier, we are a Clio Certified Partner, MyCase Partner, and QuickBooks Online ProAdvisor. The Clio QuickBooks integration is one piece of our Legal Ledger Protocol. We configure the integration, handle the trust transactions it cannot sync, and perform weekly three-way reconciliation so your books are audit-ready by the 10th of each month.

What the Integration Cannot Do

The Clio QuickBooks integration moves data between systems. That's it. It does not:

Categorize your expenses

Reconcile your bank accounts

Verify trust account reconciliation (three-way reconciliation requires a human reviewing three different reports)

Catch silent sync failures

Produce accurate financials from inaccurate inputs

Know anything about your bar's trust accounting rules

The integration is infrastructure. Someone still needs to verify the sync completed, reconcile accounts monthly, record trust transactions correctly, and catch discrepancies before they compound into the $47,000 problems we opened with.

For firms handling client funds, that someone needs to understand both the software and the rules. California requires client ledger cards with running balances and California-based bank accounts. New York requires attorney attestations on trust transactions and separate escrow accounts for real estate matters. Texas allows interest-bearing trust accounts with specific allocation requirements. Florida mandates six-year record retention with prescribed reconciliation formats. The integration does not track any of this. Your bar's random audit program does not care that your sync ran successfully.

How We Handle This

At Accounting Atelier, we configure Clio QuickBooks integrations as part of our Legal Ledger Protocol™ - a trust accounting compliance system built for firms that handle client funds. The integration handles operating transaction sync. We handle everything it can't:

Daily trust account monitoring

Weekly three-way reconciliation between bank, QuickBooks, and Clio

Monthly compliance review against your bar's specific requirements

Quarterly audit-readiness checks

The integration is one piece. If you want the whole system - someone who has fixed the problems above and knows how to prevent them - law firm bookkeeping is what we do.

Accounting Atelier provides law firm bookkeeping and trust accounting compliance for law firms. Clio Certified Partner. QuickBooks Online ProAdvisor. We configure integrations that actually work.

Frequently Asked Questions

-

QuickBooks Online can track IOLTA funds, but it is not a trust accounting system. It will not prevent you from overdrawing a client balance, generate three-way reconciliation reports, or produce the audit-formatted trust ledgers most state bars require. You need to set up a separate IOLTA bank account in your chart of accounts, create a trust liability account with client-level sub-accounts (required in California, New York, Texas, and Florida), and build manual workflows for every trust transaction. QuickBooks handles the tracking if configured correctly. The compliance, reconciliation, and oversight still require a bookkeeper who understands Rule 1.15 and your state bar's specific requirements.

-

Solo and small law firms typically use QuickBooks Online for general bookkeeping paired with a practice management platform like Clio or MyCase for billing and client tracking. Some firms add LeanLaw as middleware between Clio and QuickBooks for better trust transaction handling. All-in-one platforms like CosmoLex include built-in legal accounting and trust features but lack the general ledger depth of QuickBooks. The right setup depends on trust volume and complexity. For firms with active IOLTA accounts, the combination of Clio for practice management, QuickBooks Online Plus or Advanced for accounting, and a bookkeeper who handles the trust transactions the integration cannot sync is the configuration that works at scale.

-

Both Clio and MyCase integrate with QuickBooks Online to sync invoices and operating payments. Neither handles trust accounting through the integration. The configuration requirements are nearly identical: separate operating and IOLTA bank accounts in QuickBooks, trust liability sub-accounts by client, proper income account mapping, and manual trust transaction entry. Where they differ is ecosystem. Clio has a larger app directory and more third-party integrations. MyCase includes built-in payment processing that some firms prefer. For bookkeeping purposes, the practice management platform matters less than the QuickBooks configuration and the trust workflows your bookkeeper builds around it. At Accounting Atelier, we are certified partners with both Clio and MyCase and configure the integration the same way for either platform.

-

The Clio QuickBooks integration does not sync trust transactions, and this is by design. Trust accounting requires controls that automated sync does not provide. To handle trust accounting alongside the integration, configure QuickBooks with a separate IOLTA bank account and trust liability sub-accounts by client, then build manual workflows for trust deposits, trust-to-operating transfers, and client liability adjustments. The integration handles operating transactions (invoices, payments, contact data). Every trust entry in QuickBooks must be recorded separately by someone who understands your state bar's trust accounting rules. Monthly three-way reconciliation between your IOLTA bank statement, the QuickBooks trust ledger, and individual client balances in Clio is required regardless of the integration.

-

In Clio Manage, go to Settings, then Bill Syncing, and click Connect next to QuickBooks Online. Authorize the connection with your Intuit login. The technical connection takes less than ten minutes. Before connecting, your QuickBooks file needs separate bank accounts for operating and IOLTA, a trust liability account with client-level sub-accounts (required in California, New York, Texas, and Florida), and income accounts mapped to your Clio billing categories. After connecting, four decisions matter: set invoice sync to batch rather than real-time, create separate payment methods for operating payments and trust applications, set contact sync to one-way from Clio to QuickBooks, and use bank feeds in QuickBooks only. These configuration choices determine whether the integration helps your practice or creates months of cleanup.

-

CosmoLex includes built-in trust accounting with automated three-way reconciliation, client ledger tracking, and audit-ready trust reports inside the platform. Clio handles practice management and billing but relies on QuickBooks for accounting and does not sync trust transactions through the integration. If your primary concern is trust accounting automation and you want everything in one system, CosmoLex is the more self-contained option. If you want the flexibility of QuickBooks for general firm accounting, a larger app ecosystem, and are willing to build manual trust workflows (or hire a bookkeeper who will), Clio paired with QuickBooks gives you more reporting depth. The trade-off is simplicity versus flexibility. At Accounting Atelier, we work with both platforms and configure trust accounting workflows for either setup.

-

No. The Clio QuickBooks integration syncs operating transactions only: invoices, operating payments, and contact data. Trust deposits, trust-to-operating transfers, and client-level trust ledger entries must be recorded manually in QuickBooks by someone who understands your state bar's Rule 1.15 requirements. Monthly three-way reconciliation between your IOLTA bank statement, the trust ledger in QuickBooks, and individual client balances in Clio is still required regardless of the integration. This is by design. Automated trust sync without proper controls creates the kind of discrepancies that trigger bar audits.

-

Use bank feeds in QuickBooks only, not in both Clio and QuickBooks. Running dual bank feeds creates duplicate transactions that take hours to untangle. When synced payments appear in your QuickBooks bank feed, use the match function rather than categorizing them as new transactions. Before enabling the integration on an existing QuickBooks file, clear any manually entered invoices for clients managed in Clio. One rule going forward: invoices originate in Clio, period. Anyone working in QuickBooks needs to know that synced records should be matched, not re-entered.

-

Not cleanly. When a payment splits between a trust application and an operating deposit, the integration handles the operating portion but the trust portion requires manual entry in QuickBooks. You need to record the bank transfer from IOLTA to operating and reduce the client's trust liability sub-account separately. If both portions flow through the same payment path, your operating account will show cash that is not actually there. Create separate payment methods in Clio for operating payments and trust applications to keep the workflows distinct.

-

QuickBooks Online Plus or Advanced. The integration works with all QBO plans including Simple Start, but Simple Start lacks class and project tracking, which law firms need for matter-level reporting and practice area profitability. Simple Start also does not support the Accountant User role, which limits bookkeeper access. Plus gives you per-matter cost tracking, practice area reporting, and multi-user access. Advanced adds custom fields and enhanced reporting for firms that need more granular data. For firms using Clio with an external bookkeeper, Plus is the minimum plan that supports both the integration and proper bookkeeper access.

-

Check the connection status in Clio under Settings, then Bill Syncing. Authorization tokens expire, especially when two-factor authentication is enabled. Re-authorize the connection, then manually sync any invoices created during the gap. Build a weekly verification into your workflow: compare invoice counts between Clio and QuickBooks to catch silent sync failures before they compound into reconciliation problems.

-

If your trust accounting is simple (a handful of clients, minimal trust activity, one IOLTA account), careful DIY setup can work. Create your mapping document, plan your trust workflows, and read through the full configuration steps before connecting. If you have significant trust volume, multiple accounts, or a QuickBooks file that needs cleanup first, professional configuration prevents the compounding errors that take weeks to untangle. The $47,000 trust discrepancy described above took longer to fix than proper setup would have taken.