Accounting for Law Firms: The Complete Guide from a Legal Bookkeeper (2026)

Law firm accounting is not regular small business accounting. The difference is trust accounting: the legal and ethical obligation to track, segregate, and document every dollar of client money that passes through your firm. A restaurant tracks revenue and expenses. A law firm tracks revenue, expenses, and other people's money held in a fiduciary capacity, with the state bar watching.

If you are a solo or small firm attorney handling your own books, or working with a general bookkeeper who has never reconciled a trust account, this guide covers every part of the accounting process that matters for your firm, your license, and your compliance. For the hands-on bookkeeping side, see our companion guide to bookkeeping for law firms.

Why Law Firm Accounting Is Different

Three things separate law firm accounting from every other type of small business accounting.

Trust accounting and IOLTA requirements. When a client pays a retainer, that money does not belong to you until you earn it. It belongs to the client and must be held in a separate Interest on Lawyers Trust Account (IOLTA) until fees are earned or expenses are incurred. ABA Model Rule 1.15 requires that all client property be kept separate from your personal and business property. Every state has adopted some version of this rule, and the specifics vary. In California, for example, Business and Professions Code section 6211 requires attorneys who handle client funds to maintain trust accounts at approved financial institutions. In New York, Disciplinary Rule 9-102 (22 NYCRR 1200.46) governs the same obligation.

This is a fiduciary responsibility. The bar does not treat trust accounting violations the way the IRS treats a late tax filing. Mishandling client funds can result in suspension or disbarment.

Dual accounting structure. Every law firm operates with at least two bank accounts that must be kept completely separate: an operating account for the firm's own money (revenue, expenses, payroll) and a trust account (IOLTA) for client funds. Many firms also maintain a separate business savings account. The operating and trust accounts are two distinct financial universes. Money moves from trust to operating only when fees are earned, through a documented transfer. No exceptions.

Bar oversight and audit risk. State bars actively monitor trust accounts. California launched the Client Trust Account Protection Program (CTAPP) in 2025, giving the State Bar authority to audit any attorney's trust accounting records without a client complaint and without probable cause. The first 100 random audits began in late 2025, with the CTAPP reporting deadline set for March 30, 2026. In New York, banks are required to report dishonored checks or overdrafts on attorney trust accounts directly to the Grievance Committee under 22 NYCRR Part 1300. Florida requires similar overdraft notification to the Florida Bar, and attorneys must certify annually that they comply with IOTA rules.

This is not theoretical. If you handle client funds, your trust accounting is subject to review at any time, in most states, with or without a complaint.

The Monthly Accounting Process for a Law Firm

A complete monthly close for a law firm has more steps than a typical small business because of the trust accounting layer. Here is what the process looks like, in order.

Step 1: Operating account transaction categorization. Every transaction in the firm's operating account gets categorized: legal fee revenue, consultation fees, office rent, malpractice insurance premiums, bar dues, CLE expenses, court costs, software subscriptions, payroll. This is the part that looks like normal small business bookkeeping.

Step 2: Trust account reconciliation. This is the step that separates law firm accounting from everything else. A proper trust reconciliation is a three-way reconciliation, meaning three numbers must match:

The bank statement balance for the trust account

The trust account ledger balance (your books)

The sum of all individual client ledger balances

If those three numbers do not match, something is wrong. It could be a timing difference (a deposit that has not cleared), a data entry error, or something more serious like a commingling issue or unauthorized transfer. The reconciliation identifies it.

This is not optional. ABA Model Rule 1.15 requires lawyers to maintain current books and records in accordance with generally accepted accounting practice. Most state bars require monthly trust reconciliation, and some (like California under CTAPP) now require documentation that proves you are doing it.

Step 3: Earned fee transfers. When work has been performed and the fee has been earned, the corresponding amount transfers from the trust account to the operating account. Each transfer must be documented: the client, the matter, the amount, the date, and the invoice or billing entry it corresponds to. This is not a bulk transfer. Each earned fee moves individually, tied to specific work.

Step 4: Accounts receivable review. Review outstanding invoices. According to the 2025 Clio Legal Trends Report, the average collection rate for law firms is 93%, but the average utilization rate is only 38%. That means attorneys are billing for fewer than half their available hours and losing another 7% of what they do bill. Monthly AR review catches aging invoices before they become write-offs.

Step 5: Financial statement preparation. Three reports, every month:

The Profit and Loss statement (P&L) shows revenue minus expenses for the period. The Balance Sheet shows what the firm owns, what it owes, and the owner's equity. The Cash Flow statement shows where money came from and where it went. For firms with trust accounts, the Balance Sheet should reflect trust liabilities as a separate line item, not mixed into operating liabilities.

Step 6: IOLTA compliance documentation. File the month's trust reconciliation report, client ledger summaries, and earned fee transfer records. If California, confirm CTAPP reporting is current. If your state bar calls, this is the documentation they ask for first.

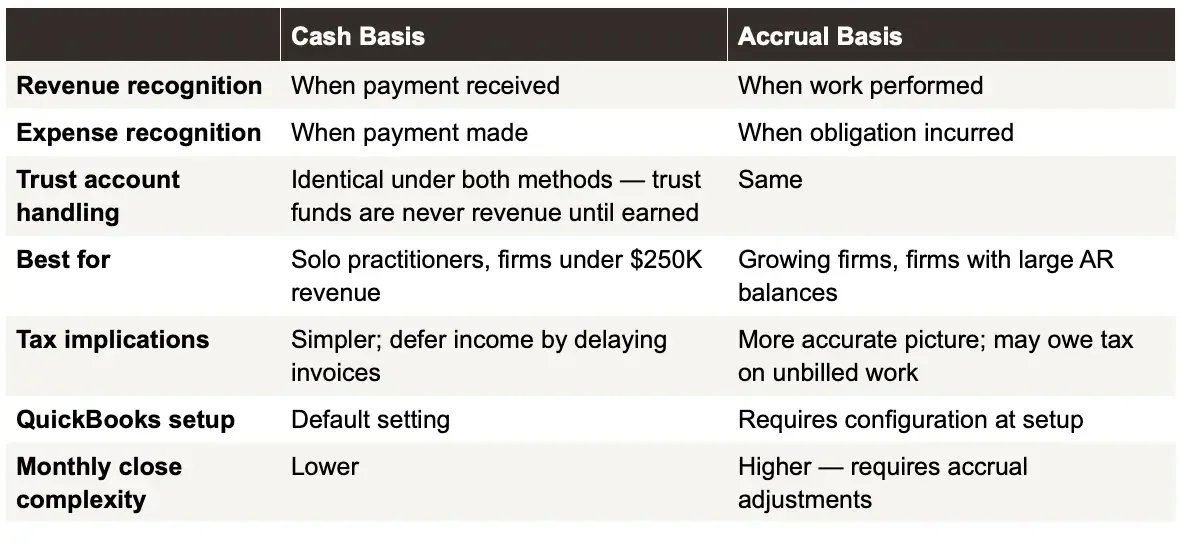

Cash Basis vs. Accrual Accounting for Law Firms

Most solo and small law firms use cash basis accounting, and for good reason: it is simpler, it aligns with how most small firms experience their cash flow, and the IRS allows it for businesses with average annual gross receipts under $31 million (the 2025 threshold, adjusted annually for inflation). Virtually every solo and small law firm falls well under that number.

When cash basis works: Cash basis records revenue when payment is received and expenses when they are paid. For a solo attorney billing hourly or flat fee and collecting within 30 to 60 days, cash basis gives an accurate picture of the firm's financial position. It is also easier to maintain, which matters when you are managing your own books or working with a part-time bookkeeper.

When accrual makes sense: Accrual accounting records revenue when earned (not when collected) and expenses when incurred (not when paid). This matters for firms with significant work-in-progress (WIP), large receivables balances, or multiple attorneys where the timing gap between work performed and payment received is substantial. If your firm regularly has $50,000 or more in unbilled WIP, accrual accounting gives a more accurate picture of the firm's actual financial position.

The trust accounting interaction: Regardless of whether your firm uses cash or accrual, trust funds are never revenue until earned. A $10,000 retainer deposited into your IOLTA account is a liability on your Balance Sheet, not income. It becomes revenue only when you perform the work, transfer the earned portion to your operating account, and record the corresponding income entry. This is true under both methods, and getting it wrong is one of the most common accounting mistakes law firms make.

Chart of Accounts for Law Firms

Your chart of accounts is the organizational framework for every transaction your firm records. A generic QuickBooks setup, the kind that comes out of the box for "Professional Services," does not account for trust liabilities, IOLTA requirements, or the dual-account structure that law firms operate under.

A legal-specific chart of accounts includes:

Income accounts broken out by type: legal fees (hourly), legal fees (flat fee), legal fees (contingency), consultation fees, and recovered costs. If the firm handles multiple practice areas, income should be tracked by practice area so you can see profitability for each one.

Trust liability accounts for the IOLTA account: a parent trust liability account with sub-accounts or class tracking for individual client matters. This is what makes the three-way reconciliation possible. Every dollar in trust is tied to a specific client and a specific matter.

Operating expense accounts specific to law practice: malpractice insurance, bar association dues, CLE (continuing legal education) costs, court filing fees, expert witness fees, legal research subscriptions (Westlaw, LexisNexis), practice management software, professional development, and attorney referral fees. These categories do not exist in a standard small business chart of accounts.

Owner's equity accounts including owner's draws and owner's contributions, which are especially important for solo practitioners operating as sole proprietorships or single-member LLCs.

If your current chart of accounts does not have a separate trust liability section, your books are not set up correctly for law firm accounting. A bookkeeper who specializes in law firms can restructure this without losing your historical data.

Software for Law Firm Accounting

Law firm accounting typically runs on two systems working together: an accounting platform and a practice management platform.

QuickBooks Online is the accounting backbone for the majority of solo and small law firms. It handles the general ledger, bank reconciliation, financial statements, and tax-related reporting. It is not built for trust accounting, which is why it needs a practice management platform connected to it.

Practice management platforms like Clio, MyCase, PracticePanther, and Smokeball handle time tracking, billing, invoicing, and client matter management. These platforms sync billing and payment data to QuickBooks, which is where the trust accounting integration becomes critical. If the sync is not configured correctly, trust transactions end up miscategorized in QuickBooks, and your financials are wrong.

CosmoLex takes a different approach by building accounting directly into the practice management platform, eliminating the need for a separate QuickBooks account. This can simplify the workflow for firms that want one system, though it means giving up the flexibility and integrations that QuickBooks provides.

The choice of software matters less than the configuration. Any of these platforms can produce clean financials if set up correctly. The majority of trust accounting problems trace back to configuration, not the software itself.

For a full comparison of platforms, see our guide to the best accounting software for law firms. For trust-specific software, see the best IOLTA trust accounting software for law firms. If you are already on Clio, see how the Clio and QuickBooks integration should be configured.

When to Hire a Legal Bookkeeper vs. Doing It Yourself

There are parts of law firm accounting you can handle yourself, and parts you should not.

What you can manage: Basic expense tracking, creating and sending invoices, logging time entries, and reviewing your monthly financial statements once they are prepared. These are operational tasks that do not require specialized accounting knowledge.

What you should hand off: Trust account reconciliation, three-way reconciliation, IOLTA compliance documentation, earned fee transfer tracking, chart of accounts configuration, and QuickBooks-to-practice-management sync management. These tasks require specific knowledge of legal accounting rules, and errors have consequences beyond a messy P&L. They can trigger bar complaints, audits, or worse.

The distinction between a legal bookkeeper and a general bookkeeper matters here. A general bookkeeper can categorize your expenses and reconcile your operating account. A legal bookkeeper understands trust accounting, knows the difference between an IOLTA liability and operating revenue, and can prepare the documentation your state bar requires.

According to the 2025 Clio Legal Trends Report, the average attorney bills at $349 per hour. Every hour you spend reconciling your own trust account is an hour you are not billing. At that rate, a bookkeeper who costs $500 to $1,500 per month pays for themselves in recovered billing time within the first week.

For more on this decision, see when to outsource your law firm bookkeeping and what law firm bookkeeping actually costs.

Common Accounting Mistakes Law Firms Make

These are the mistakes I see most often. All of them are preventable.

Commingling trust and operating funds. Depositing personal or firm money into the trust account, or using trust funds for operating expenses before fees are earned. This is the single fastest path to a bar complaint. ABA Model Rule 1.15 allows only one exception: you may deposit a small amount of your own funds into the trust account to cover bank service charges. Nothing else.

Skipping monthly trust reconciliation. Some firms reconcile quarterly, or only when they "have time." Trust accounts need monthly reconciliation at minimum. California's CTAPP now requires documentation proving you are doing it. If a discrepancy exists and you do not catch it for three months, the problem compounds and the explanation to the bar gets harder.

Using a general bookkeeper who does not understand IOLTA. A bookkeeper who treats your trust account like a second operating account will miscategorize trust deposits as income, miss earned fee transfers, and produce financials that look correct but are fundamentally wrong. Your books can balance to the penny and still fail a bar audit.

No separation between personal and business finances. Solo practitioners sometimes run firm expenses through personal accounts, or vice versa. This creates problems at tax time, makes trust accounting harder to verify, and raises red flags if your books are ever reviewed.

Not tracking retainers as liabilities. A client retainer deposited into your IOLTA account is not revenue. It is a liability until the corresponding work is performed. If your books record retainer deposits as income on receipt, your revenue is overstated and your trust liability is understated. This is both an accounting error and a compliance issue.

Missing earned fee transfers. Work gets done, invoices go out, but the earned fees sit in the trust account instead of being transferred to operating. This leaves client money sitting in trust longer than it should, and it makes your operating account look less profitable than it actually is.

For a deeper look at trust accounting errors, see the most common IOLTA compliance mistakes.

What Good Law Firm Accounting Looks Like

When a law firm's accounting is working the way it should, it looks like this:

Monthly financial statements, including P&L, Balance Sheet, and Cash Flow, delivered by the 15th of the following month. Trust account reconciled to the penny every month, with a three-way reconciliation report on file. Documentation for every earned fee transfer from trust to operating. Clean separation between trust liabilities and operating revenue on the Balance Sheet.

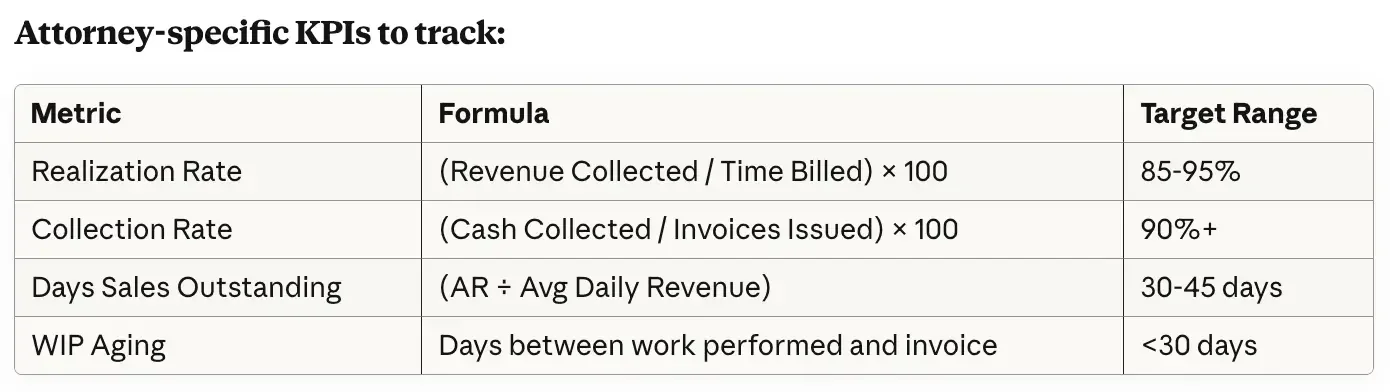

The firm knows its profitability by practice area. The firm knows its average collection period and realization rate. The firm knows exactly how much money is in trust, who it belongs to, and why it is there. There are no surprises at tax time because the books have been accurate all year.

This is not aspirational. This is the baseline for any firm that handles client funds and wants to stay in compliance.

For benchmarks on what healthy law firm financials look like, see law firm financial benchmarks and the metrics every law firm should track.

What High-Level Bookkeeping for Law Firms Provides Monthly

Outsourced bookkeeping for law firms delivers more than transaction processing. Specialized providers act as financial operations partners, handling compliance workflows and surfacing insights that inform strategy.

Monthly deliverables from specialized legal bookkeeping:

Transaction and reconciliation services:

Complete bank and credit card reconciliations with discrepancies investigated

IOLTA 3-way reconciliation executed and documented

Trust liability report generated and verified

Matter ledger maintenance with all transactions properly allocated

Expense categorization using law firm chart of accounts

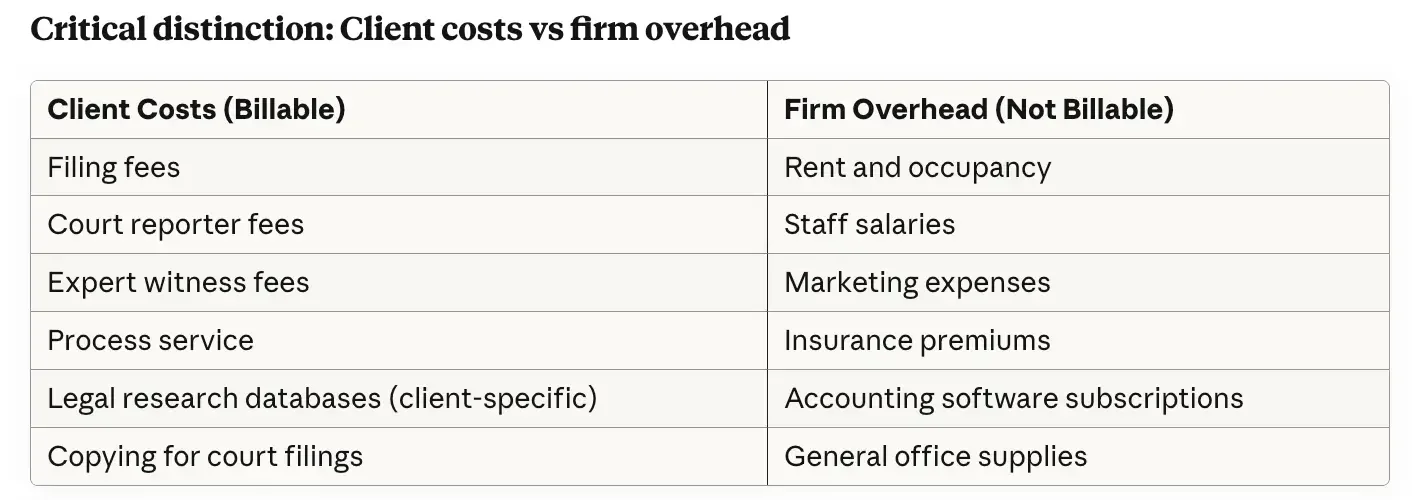

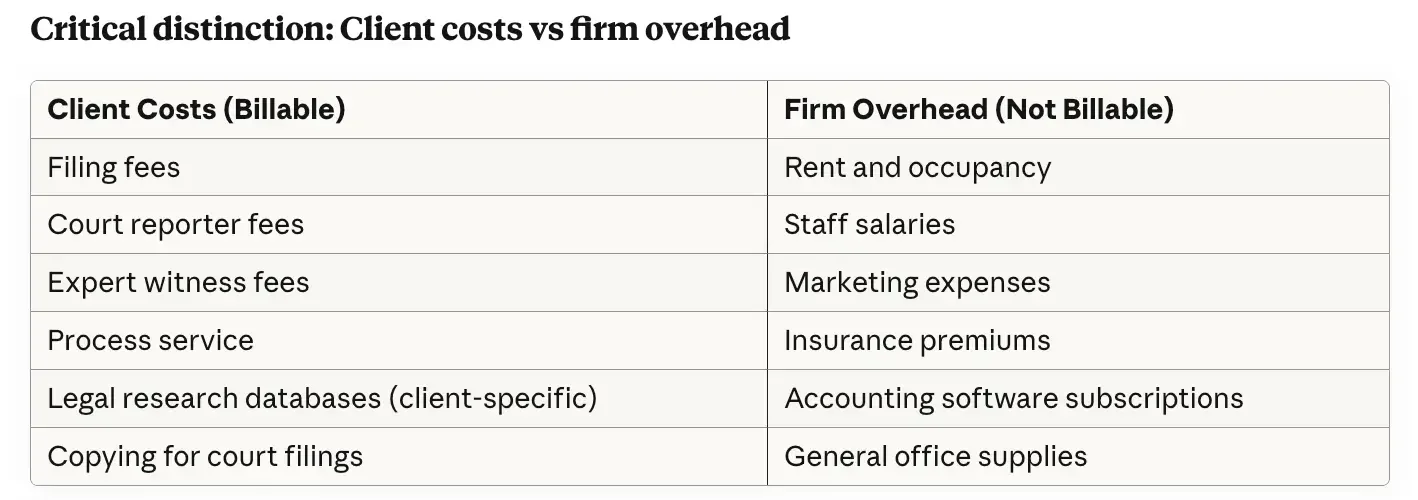

Client cost allocation to specific matters

Accounts payable processing with proper coding

Compliance and documentation:

Trust accounting compliance procedures followed monthly

Documentation package supporting trust reconciliation

Negative client balance monitoring and alerting

Stale retainer identification and reporting

Compliance checkpoint verification

Audit-ready trust accounting records maintained

Reporting and analysis:

Monthly financial statement package (P&L, balance sheet, cash flow)

Trust liability report with client balance detail

Matter-level profitability reporting

Accounts receivable aging analysis

Work-in-progress aging report

Key law firm financial metrics calculated

Delivered by 10th-15th of following month consistently

Strategic support:

Proactive communication about unusual transactions

Identification of compliance risks before they become violations

Recommendations for process improvements

Financial performance insights based on metrics trending

Matter profitability analysis and observations

Cash flow forecasting and runway monitoring

The goal extends beyond clean books to creating financial operations infrastructure that supports growth without creating risk.

Understanding pricing structures and what's included at different service levels helps firms budget appropriately. Learn more about law firm bookkeeping costs and typical monthly packages.

Ready to Build Financial Operations That Match Your Legal Standards?

Law firm accounting demands the same rigor attorneys apply to client matters. The monthly financial workflow outlined here creates infrastructure for compliance, profitability, and confident growth.

Professional financial operations separate law firms that scale successfully from those constrained by back-office chaos. Clean books, compliant trust accounting, and matter-level visibility provide the foundation for strategic decisions.

If you want your law firm's accounting handled with the same care you give your cases, let's talk numbers.

Frequently Asked Questions

-

Law firm accounting is the process of tracking, recording, and reporting a law firm's financial transactions, including both operating revenue and expenses and client trust funds held in IOLTA accounts. It differs from standard small business accounting because of the fiduciary obligation to manage client money separately under bar rules and ABA Model Rule 1.15.

-

The primary difference is trust accounting. Law firms hold client money in IOLTA trust accounts that must be tracked separately from the firm's operating funds. This creates a dual accounting structure with compliance requirements enforced by state bar associations, including mandatory reconciliation, documentation, and reporting obligations that do not apply to other businesses.

-

Trust accounting is the process of tracking client funds held in an IOLTA account, including retainers, settlement proceeds, and other client money. It matters because these funds belong to the client until fees are earned, and the attorney has a fiduciary duty to safeguard them. Mishandling trust funds is one of the leading causes of attorney discipline, including suspension and disbarment.

-

Three-way reconciliation is a monthly process that compares three numbers: the bank statement balance for the trust account, the trust ledger balance in your books, and the total of all individual client ledger balances. All three must match. If they do not, there is either an error or a compliance problem that needs to be identified and resolved. For a full walkthrough, see three-way reconciliation for law firms.

-

Most solo and small law firms need both, but for different functions. A bookkeeper handles the day-to-day financial work: transaction categorization, trust reconciliation, monthly financial statements, and IOLTA compliance documentation. A CPA handles tax planning, tax preparation, and strategic financial advice. The bookkeeper should specialize in law firms. The CPA should be familiar with legal industry tax considerations.

-

Most solo and small law firms use QuickBooks Online for their general ledger and financial reporting, paired with a practice management platform like Clio, MyCase, or PracticePanther for time tracking, billing, and trust accounting. The integration between the two systems matters more than the specific software choice. CosmoLex combines both functions in one platform. See the best accounting software for law firms for a full comparison.

-

Law firm bookkeeping typically costs between $500 and $1,500 per month for a solo or small firm, depending on transaction volume, the number of trust accounts, and the complexity of the billing structure. A CPA for tax preparation adds $1,000 to $5,000 annually. See law firm bookkeeping costs for a detailed breakdown.

-

IOLTA stands for Interest on Lawyers Trust Account. It is the account where attorneys hold client funds that are too small or held too briefly to earn interest for the individual client. Instead, the interest is pooled and directed to state legal aid programs. IOLTA affects your accounting because every transaction in that account must be tracked by client and by matter, reconciled monthly, and documented for potential bar review. See the complete IOLTA account guide.

-

Monthly, at minimum. The operating account should be reconciled to the bank statement monthly, just like any business. The trust account requires a full three-way reconciliation every month: bank balance, trust ledger balance, and individual client ledger balances. Some state bars, including California under CTAPP, now require documentation proving that monthly reconciliation is being performed.

-

The consequences range from minor to career-ending, depending on the nature and severity of the error. Unintentional bookkeeping errors may result in a letter of caution or requirement to complete a trust accounting course. Commingling client funds with firm funds, or failing to maintain adequate trust records, can result in formal discipline including public reprimand, suspension, or disbarment. In California, a trust accounting deficiency identified through the CTAPP random audit program triggers a compliance review that can escalate to formal investigation. See attorney trust account rules by state.

If your firm's accounting is working well, you already know it. If you are not sure, or if the words "three-way reconciliation" do not describe something you do every month, it is worth having someone who specializes in law firm bookkeeping take a look.

Schedule a consultation about your firm's bookkeeping or, if your trust account needs immediate attention, see our trust account cleanup service.