Bookkeeping for Law Firms: What It Includes and Why It's Different (2026)

Updated March 2026

Law firm bookkeeping is bookkeeping plus trust accounting. That one addition changes everything: what gets tracked, how accounts are reconciled, what documentation is required, and what happens when something goes wrong. A bookkeeping error at a restaurant means a messy tax return. A bookkeeping error at a law firm can mean a bar complaint, a disciplinary hearing, or a suspended license.

If you are a solo or small firm attorney handling your own books, working with a general bookkeeper who has never touched an IOLTA account, or trying to figure out whether your current bookkeeping is actually protecting you, this guide walks through every part of the process. For the broader strategic picture of how law firm accounting works as a system, see our companion guide to accounting for law firms.

What Law Firm Bookkeeping Actually Includes

A complete law firm bookkeeping process covers nine recurring tasks every month. Not all of them happen at every firm, but if your firm handles client funds, all nine apply to you.

1. Transaction categorization for operating accounts. Every deposit and payment in the firm's operating account gets categorized: legal fee revenue by type, consultation income, office rent, malpractice insurance, bar dues, CLE costs, court filing fees, software subscriptions, meals, mileage, payroll. This is the work that looks the same as any small business. It is also the part most solo attorneys try to handle themselves, often by ignoring it until tax season.

2. Trust account deposit recording. Every client retainer, settlement fund, or advance cost deposit into the IOLTA account gets recorded with the client name, matter number, date, and purpose. Each deposit creates or adds to a client-specific ledger within the trust account. There is no bulk deposit category. Every dollar in trust is tied to a person and a case.

3. Trust account disbursement tracking. When money leaves the trust account, whether as an earned fee transfer, a client refund, a cost payment, or a settlement distribution, the disbursement gets recorded against the correct client ledger with documentation showing who authorized it and why.

4. Three-way trust reconciliation. This is the task that defines law firm bookkeeping. Once a month, three numbers must match: the bank statement balance for the trust account, the trust ledger total in your books, and the sum of all individual client ledger balances. If they do not match, the discrepancy must be identified and resolved before the books close. This is not a general reconciliation where you match deposits and checks. It is a three-sided verification that every dollar in trust belongs where you say it does. For the full process, see three-way reconciliation for law firms.

5. Earned fee transfers. When you perform legal work and bill for it, the earned portion moves from the trust account to the operating account. Each transfer is documented individually: the client, the matter, the amount, the corresponding invoice, and the date. Batch transfers with no documentation are a compliance problem.

6. Accounts receivable tracking. Review outstanding invoices, identify aging balances, and follow up. According to the 2025 Clio Legal Trends Report, the average law firm collection rate is 93%, but the average utilization rate is only 38%. That means attorneys are billing for fewer than four hours out of every eight-hour day and losing another 7% of what they do bill. Consistent AR follow-up is the difference between revenue earned and revenue collected.

7. Accounts payable and bill payment. Vendor invoices, bar dues, insurance premiums, subscription renewals, court costs, expert witness fees. For solo practitioners, this often gets handled informally. Formal AP tracking prevents missed payments and keeps your expense records clean for tax reporting.

8. Monthly financial statement preparation. Three reports, every month. The Profit and Loss statement shows what the firm earned and spent. The Balance Sheet shows assets, liabilities (including trust account balances), and owner's equity. The Cash Flow statement shows the actual movement of money in and out of the firm. These should be delivered by the 10th to 15th of the following month.

9. IOLTA compliance documentation. The month's trust reconciliation report, client ledger summaries, earned fee transfer records, and any trust account bank statements get filed as compliance documentation. This is the paper trail your state bar will request if your trust account is audited. In California, the Client Trust Account Protection Program (CTAPP) now requires this documentation as part of its random audit process, with the reporting deadline set for March 30, 2026. In New York, banks report any dishonored checks or overdrafts on attorney trust accounts directly to the Grievance Committee under 22 NYCRR Part 1300. Florida requires annual written certification of IOTA compliance.Trust Accounting (The Non-Negotiable Difference)

Trust Accounting: The Part That Makes Law Firm Bookkeeping Different

Every section above that mentions "trust" is the reason a general bookkeeper cannot do this work without training. Trust accounting is not just another account to reconcile. It is a separate financial system governed by ethics rules, not just tax law.

Why it exists. Attorneys hold other people's money. Retainers, settlement proceeds, real estate escrow funds, advance cost deposits. ABA Model Rule 1.15 requires that these funds be kept in a separate account from the attorney's own money and that the attorney maintain current records and provide accountings on request. Every state has adopted some version of this rule. It is the foundation of the fiduciary duty attorneys owe to their clients. For a complete overview of IOLTA requirements, see the IOLTA account guide.

What three-way reconciliation proves. The monthly reconciliation does not just verify that the bank balance matches your books. It verifies that every dollar in the trust account can be attributed to a specific client and a specific matter. If you have $47,000 in trust and 12 active client matters, the individual client ledgers must add up to exactly $47,000, and that total must match both your trust ledger and the bank statement. Three numbers. One answer.

Per-client and per-matter ledgers. Trust accounting requires sub-ledger tracking for each client, and in many cases, for each matter within a client relationship. An attorney handling a personal injury case and an estate matter for the same client needs separate trust ledgers for each. Funds cannot be moved between matters without proper documentation and client authorization.

Earned vs. unearned fees. A $5,000 retainer deposited into trust is a liability, not revenue. The firm owes that money to the client until work is performed. As hours are billed and invoiced, the earned portion transfers to operating, and only then is it recognized as revenue. Getting this timing wrong is one of the most common compliance errors, and one of the most dangerous. See common IOLTA compliance mistakes for the full list.

What happens when trust accounting goes wrong. Trust accounting violations are among the leading causes of attorney discipline across every jurisdiction. In California, CTAPP gives the State Bar authority to randomly audit any attorney's trust records without a complaint. In New York and Florida, overdraft reporting triggers immediate scrutiny. Consequences range from letters of caution for minor errors to public reprimand, suspension, or disbarment for commingling or misappropriation. For a state-by-state breakdown, see attorney trust account rules.

The Monthly Bookkeeping Cycle for a Law Firm

A well-run monthly close follows a predictable sequence. Here is how the month typically works for a solo or small firm attorney working with a dedicated legal bookkeeper.

Week 1 (1st through 7th): Data collection and transaction recording. The bookkeeper downloads bank and credit card feeds for the prior month, categorizes operating transactions, and records all trust account deposits and disbursements. Any uncategorized transactions get flagged for the attorney. Client trust ledgers are updated with the prior month's activity.

Week 2 (8th through 14th): Reconciliation. Operating account reconciliation happens first: matching the bank statement against the general ledger, identifying any discrepancies, and clearing them. Then the trust account three-way reconciliation: bank balance, trust ledger, and individual client ledgers. If the three-way reconciliation does not balance, the bookkeeper traces the discrepancy before moving forward. Nothing else closes until trust is reconciled.

Week 3 (15th through 21st): Financial statements and AR review. The P&L, Balance Sheet, and Cash Flow statement are prepared. The bookkeeper reviews accounts receivable aging, flags invoices over 30, 60, and 90 days, and provides the attorney with a summary. This is also when the bookkeeper prepares the trust account summary showing balances by client and by matter.

Week 4 (22nd through end of month): Delivery and compliance filing. Financial statements and the trust reconciliation report are delivered to the attorney. IOLTA compliance documentation is filed. Any items requiring the attorney's attention (unusual transactions, client overpayments in trust, aging receivables) are flagged in a brief summary.

For context on what healthy numbers look like in those reports, see law firm financial benchmarks.

The whole process should be invisible to you by week 4. You review the reports, ask questions if something looks off, and get back to practicing law. If your current bookkeeping process requires you to chase down your own bank statements, answer dozens of categorization questions, or wonder whether your trust account is reconciled, the system is not working the way it should.

For a complete breakdown of monthly deliverables, see law firm bookkeeping reports every managing partner needs.

DIY Bookkeeping vs. Outsourcing

There are parts of law firm bookkeeping you can handle. There are parts you should not.

What a solo attorney can realistically manage: Creating and sending invoices from your practice management platform, logging time entries as you work, tracking basic expenses by photographing receipts or connecting a bank feed to QuickBooks, and reviewing financial statements once they are prepared. These tasks do not require specialized knowledge. They require consistency, which is the harder part.

What requires a legal bookkeeper: Trust account reconciliation, three-way reconciliation, IOLTA compliance documentation, earned fee transfer tracking and documentation, and the monthly financial close. These tasks require someone who understands the difference between an IOLTA liability and operating revenue, who knows how Rule 1.15 applies in your state, and who has reconciled trust accounts before. A mistake here is not a tax inconvenience. It is a compliance risk.

The real cost of doing it yourself. The 2025 Clio Legal Trends Report puts the average attorney billing rate at $349 per hour. If trust reconciliation takes you three hours a month (and it often takes longer if you are not practiced at it), that is over $1,000 in lost billing time. Add the risk of a compliance error that triggers a bar inquiry, and the math gets worse quickly.

When outsourcing makes sense. If your firm handles any client funds in trust, outsourcing trust accounting to a legal bookkeeper is worth evaluating. If you find yourself doing your books on weekends, catching up on categorization at tax time, or wondering whether your trust account is actually reconciled, those are signals that the current system is costing you more than a bookkeeper would. For a deeper analysis of this decision, see when to outsource your law firm bookkeeping and the hidden cost of DIY bookkeeping.

What to Look for in a Law Firm Bookkeeper

Not every bookkeeper can do this work. The skill set required for law firm bookkeeping is specific enough that hiring the wrong person creates more problems than it solves.

Trust accounting experience is non-negotiable. A bookkeeper who has never reconciled a trust account will need to learn on your books, which means learning on your license. Ask how many law firm clients they work with. Ask them to describe a three-way reconciliation. If they cannot explain it clearly, keep looking.

QuickBooks Online proficiency. The majority of solo and small law firms run their general ledger on QBO. A QuickBooks Online ProAdvisor certification means the bookkeeper has been tested on the platform. It does not mean they know legal bookkeeping, but it confirms the technical foundation.

Practice management integration knowledge. If your firm uses Clio, MyCase, PracticePanther, or Smokeball, your bookkeeper needs to understand how billing and payment data syncs from that platform to QuickBooks. A misconfigured integration is one of the most common sources of trust accounting errors. Ask whether they have set up or managed the integration for other law firm clients.

Monthly deliverables they should provide. At minimum: P&L, Balance Sheet, Cash Flow statement, trust reconciliation report with three-way reconciliation documentation, accounts receivable aging summary, and a brief narrative noting anything that needs your attention. If a bookkeeper does not deliver trust reconciliation documentation, they are not doing law firm bookkeeping.

Red flags. No trust accounting experience with law firms. Billing hourly for routine monthly work (a fixed monthly fee aligned to your firm's complexity is standard). No other legal clients in their practice. Reluctance to discuss their trust reconciliation process. Any suggestion that trust accounting "is basically the same" as regular bank reconciliation.

For more on evaluating candidates, see the difference between a legal bookkeeper and a general bookkeeper and how to hire a law firm bookkeeper.

What Law Firm Bookkeeping Costs

Bookkeeping costs for a law firm depend on firm size, transaction volume, and trust account complexity.

DIY costs (software only): QuickBooks Online runs $35 to $100 per month depending on the plan. Add a practice management platform ($49 to $139 per user per month for Clio, $49 to $89 for PracticePanther, similar ranges for MyCase and Smokeball). Software alone runs $85 to $240 per month for a solo attorney. This covers the tools, not the labor.

Outsourced bookkeeping costs: $600 to $1,500 per month for a solo or small firm, depending on transaction volume, the number of trust accounts, and how many client matters are active. Trust-heavy firms (personal injury, real estate, estate planning) are typically at the higher end because the trust reconciliation work is more involved.

What is typically included: Monthly transaction categorization, operating account reconciliation, trust account three-way reconciliation, financial statements, IOLTA compliance documentation, and AR review. What usually costs extra: payroll processing, tax preparation (handled by a CPA), and cleanup work for firms that are behind on their books.

For a detailed breakdown with specific scenarios, see law firm bookkeeping costs.

For a deeper look at what can go wrong, see our guide to DIY bookkeeping for law firms.

Common Bookkeeping Mistakes Law Firms Make

These are the errors that come up repeatedly, across firms of every size and practice area.

Commingling trust and operating funds. Depositing firm revenue into the trust account, paying firm expenses from trust, or leaving earned fees in trust after they have been billed and collected. ABA Model Rule 1.15 is explicit: client funds and firm funds must be kept separate. The only exception is depositing a small amount of personal funds to cover bank service charges on the trust account.

Skipping monthly trust reconciliation. Quarterly reconciliation is not sufficient. A discrepancy that goes undetected for 90 days is significantly harder to trace and explain than one caught within 30 days. California's CTAPP requires documentation proving monthly reconciliation. Even in states without that requirement, monthly reconciliation is the standard of care.

Using a general bookkeeper without legal experience. A bookkeeper who treats the trust account like a second operating account will record retainer deposits as revenue, miss earned fee transfers, and produce financial statements that look clean but misrepresent the firm's actual position. The books will balance. They will not be correct.

Ignoring transactions until tax season. Categorizing a year's worth of transactions in February is damage control, not bookkeeping. Monthly categorization takes 20 minutes of review time from the attorney when a bookkeeper handles the preparation. Annual catch-up takes days and produces less accurate results.

Recording retainers as revenue before they are earned. A retainer is a liability until the corresponding work is performed. Booking it as income on receipt overstates revenue, understates trust liability, and creates a discrepancy between what your P&L says and what your trust account shows. This is both an accounting error and a bar compliance issue.

No separation between personal and business finances. Solo practitioners who run business expenses through personal accounts, or deposit client payments into personal checking, create a documentation nightmare. If your trust account is audited, the bar wants clean records. Mixing personal and business accounts makes that impossible.

For the trust-specific version of this list, see common IOLTA compliance mistakes.

For detailed pricing breakdown, see our law firm bookkeeping cost guide.

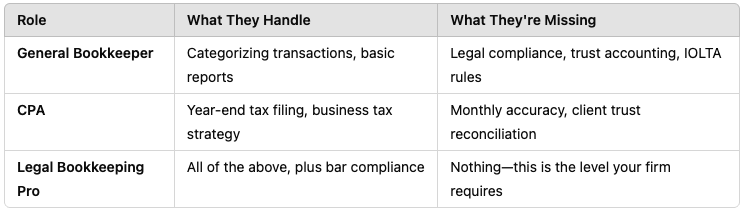

Comparison: Bookkeeper vs. CPA vs. Legal Bookkeeping Pro

Software for Law Firm Bookkeeping

Law firm bookkeeping typically runs on two platforms working together.

QuickBooks Online handles the general ledger, bank reconciliation, financial statements, and tax reporting. It is the industry standard for solo and small firms. But QBO was not designed for trust accounting. It tracks revenue and expenses. It does not track fiduciary obligations. That is why it needs a practice management platform connected to it.

Practice management platforms (Clio, MyCase, PracticePanther, Smokeball) handle time tracking, billing, invoicing, and client matter management. These platforms also handle trust accounting workflows: recording trust deposits and disbursements, maintaining client trust ledgers, and generating trust reports. Billing and payment data syncs from the practice management platform to QuickBooks.

The integration between these two systems is where most bookkeeping problems originate. If the sync is misconfigured, trust transactions get miscategorized in QuickBooks, earned fees do not transfer correctly, and your financial statements diverge from reality. A bookkeeper who understands how these systems connect can prevent this. A bookkeeper who does not will perpetuate it.

CosmoLex takes a different approach by combining accounting and practice management in one platform, eliminating the need for QuickBooks entirely. This can reduce integration issues, though it limits flexibility for firms that want QuickBooks as their accounting backbone.

For full platform comparisons, see the best accounting software for law firms and the best IOLTA trust accounting software. For QuickBooks-specific setup, see QuickBooks for law firms and how to configure the Clio-QuickBooks integration.

Not sure if you're ready? Use our decision framework for outsourcing law firm bookkeeping.

Get Your Law Firm Bookkeeping Right From Day One

Law firm bookkeeping isn't optional, and it's not something to figure out as you go. The complexity of trust accounting, the severity of compliance violations, and the time required make this a critical business function that deserves professional attention.

Whether you choose to handle it yourself with proper training and systems, or outsource to specialists who understand legal accounting, the key is having a system that maintains compliance, produces accurate reports, and supports your growth.

If your current bookkeeping setup isn't giving you confidence in your numbers and peace of mind about compliance, it's time for a change.

We specialize in bookkeeping for law firms - monthly trust reconciliation, IOLTA compliance, and financial reporting designed for legal practices. Learn more about our law firm bookkeeping services.

Book a 15-Minute Consultation. No pressure. Just clarity.

Frequently Asked Questions

-

Law firm bookkeeping is the process of recording, categorizing, and reconciling a law firm's financial transactions on a monthly basis. It includes everything standard small business bookkeeping covers (operating expenses, revenue, payroll) plus trust accounting: tracking client funds held in IOLTA accounts, performing three-way reconciliations, and maintaining the compliance documentation required by state bar associations.

-

The difference is trust accounting. Law firms hold client money in IOLTA trust accounts that must be tracked separately from firm funds, reconciled monthly using a three-way process, and documented for potential bar review. A regular bookkeeper reconciles one bank account against one ledger. A law firm bookkeeper reconciles the trust account against the bank, the trust ledger, and every individual client ledger. That additional layer of verification is what makes it a specialized discipline.

-

Trust accounting is the process of tracking every dollar of client money held in a law firm's IOLTA account. It includes recording deposits by client and matter, tracking disbursements, performing three-way reconciliations, and documenting earned fee transfers. Trust accounting exists because attorneys have a fiduciary duty under ABA Model Rule 1.15 to keep client funds separate from their own and to account for those funds at all times.

-

Monthly. The operating account should be reconciled to the bank statement every month. The trust account requires a full three-way reconciliation every month: bank balance, trust ledger balance, and individual client ledger balances. Some states, including California under its CTAPP program, now require documentation proving that monthly trust reconciliation is being performed.

-

You can handle parts of it: creating invoices, logging time, tracking expenses. The trust accounting portion, three-way reconciliation, IOLTA compliance documentation, and earned fee transfer tracking, requires specialized knowledge and carries compliance risk if done incorrectly. If your firm holds any client funds in trust, working with a bookkeeper who has law firm experience is worth the investment.

-

Outsourced law firm bookkeeping typically costs $600 to $1,500 per month for a solo or small firm, depending on transaction volume and trust account complexity. DIY costs are lower (software only, roughly $85 to $240/month) but do not account for the attorney's time spent doing the work or the compliance risk of errors in trust accounting.

-

At minimum: a Profit and Loss statement, a Balance Sheet, a Cash Flow statement, a trust account reconciliation report (showing the three-way reconciliation), an accounts receivable aging summary, and a trust balance summary showing balances by client and matter. These should be delivered by the 10th to 15th of the following month.

-

Three-way reconciliation is a monthly verification process specific to law firm trust accounts. It compares three numbers: the trust account bank statement balance, the trust ledger balance in the firm's accounting records, and the sum of all individual client ledger balances. All three must match exactly. If they do not, the discrepancy must be identified and resolved before the monthly close is complete. See three-way reconciliation for law firms for the full walkthrough.

-

Practice management platforms handle billing, time tracking, and trust accounting workflows, but they are not accounting software. They do not replace the need for a general ledger (usually QuickBooks Online), monthly financial statement preparation, or the oversight of someone who understands how the data flows between the two systems. The integration between your practice management platform and QuickBooks is where most bookkeeping errors originate.

-

It depends on what is wrong. Operating account errors (miscategorized expenses, missed deductions) create tax problems. Trust accounting errors create bar compliance problems. Commingling client funds with firm funds, failing to reconcile the trust account, or misappropriating trust funds can result in disciplinary action including public reprimand, suspension, or disbarment. In California, trust accounting deficiencies identified through CTAPP's random audit program trigger compliance reviews that can escalate to formal investigation.

If your firm's bookkeeping is running the way it should, you are not thinking about it by the third week of each month. If you are thinking about it, or if "three-way reconciliation" is not a phrase that describes something happening on your books every 30 days, it is worth a conversation.

Talk to us about your firm's bookkeeping. If your trust account needs immediate cleanup, see our trust account cleanup service.

About the Author Written by Amy Coats, founder of Accounting Atelier. With over 20 years in financial management, Amy specializes in law firm bookkeeping and IOLTA compliance. She is a QuickBooks Online ProAdvisor, Clio Certified Consultant, and MyCase Partner - dedicated to helping solo attorneys and small firms build financially sound practices.